PDF(332 KB)

PDF(332 KB)

Market Rule or Equal Opportunity Rule: An Empirical Analysis Based on Acquisitions of Chinese Listed Companies

Wenting CHEN, Wenxin LIU, Pengyi YU

系统科学与信息学报(英文) ›› 2024, Vol. 12 ›› Issue (2) : 191-211.

PDF(332 KB)

PDF(332 KB)

), Wenxin LIU(), Pengyi YU*()

), Wenxin LIU(), Pengyi YU*()

Market Rule or Equal Opportunity Rule: An Empirical Analysis Based on Acquisitions of Chinese Listed Companies

), Wenxin LIU(), Pengyi YU*()

This paper examines the data of A-share listed companies in China from 2002 to 2017, drawing on the theory of equal opportunity and market rules in M&A transactions. This paper investigates the correlation between changes in tender offer policy and M&A tendencies and performance. The findings suggest that following the policy shift and the adoption of market rules, companies that secure an exemption from the mandatory tender offer obligation not only exhibit stronger M&A tendencies but also improved long-term M&A performance. This indicates that market rules are more suitable for China and contribute to enhancing the efficiency of the M&A market. The paper also presents evidence of a moderating effect, demonstrating that exemptions from the mandatory tender offer obligation positively influence the relationship between policy change and M&A performance. Lastly, this paper finds that state-owned and large-scale firms tend to exhibit a higher degree of M&A tendencies.

takeover regulation / equal opportunity rule / market rule / mandatory tender offer {{custom_keyword}} /

Table 1 Definitions of variables |

| Variable type | Variable symbol | Variable meaning | ||

| Dependent variables | M&AC | Samples of M&A of the company in that year / Samples of all first announcements of the company in the same year | ||

| M&AT | M&AA | Make a sum of all M&A payments of the company in the year and then take its natural logarithm. | ||

| M&AP | CAR | Using CAPM model to calculate car value. The date of M&A is the date of occurrence of the event. Estimated window is | ||

| BHAR | Abnormal returns in 3 years after M&A. | |||

| MBR | Market-to-Book Ratio=total assets / market value | |||

| Independent variables | Exemption or not ( | If the company obtains the exemption, | ||

| Policy change ( | If the first announcement date is before September 2006, | |||

| Control variables | Corporate governance | Board characteristics | INDR | The proportion of the number of independent directors in the board of directors in the year before M&A. |

| Bsize | Number of board of directors in the year before M&A. | |||

| CEO chara cteristics | edu | The education background of CEO in the year of M&A, 1 for master degree or above, 0 for others. | ||

| tenure | The tenure of CEO in the year of M&A. | |||

| CEOpower | CEO compensation of the year before M&A / remuneration of directors and supervisors of the year before M&A | |||

| CEOoverconfidence | The salary of CEO in the year before M&A plus 1 and then take the natural logarithm. | |||

| Pconnection | In the year of M&A, if the CEO held the post in relevant government agencies, take it as 1, otherwise it is 0. | |||

| Executives characteristics | magshare | The proportion of shares held by board of directors and supervisors in the year before M&A. | ||

| magsalary | The total remuneration of directors and supervisors in the year before M&A plus 1 and then take the natural logarithm. | |||

| Ownership characteristics | TOP1 | The shareholding ratio of the largest shareholder in the year before M&A. | ||

| Corporate finance | lnasset | Add 1 to the total assets at the end of the year before M&A and then take the natural logarithm. | ||

| Lev | Asset liability ratio of the company in the year before M&A. | |||

| OCF | The ratio of operating cash flow to total assets in the year before M&A. | |||

| FirmGrowth | Growth rate of business income in the year before M&A. | |||

| Age | Duration of the company. | |||

| Listyear | Listing time of the company. | |||

| Others | YEAR | Annual virtual variable. | ||

| IND | Industry dummy variable. | |||

Table 2 Descriptive statistics |

| Variables | Mean | SD | Min | Max | |

| M&AC | 10879 | 0.986 | 0.076 | 0.5 | 1 |

| M&AA | 10382 | 18.603 | 2.048 | 13.122 | 23.165 |

| CAR | 186 | 0.001 | 0.065 | 0.188 | |

| BHAR | 142 | 1.345 | 7.024 | ||

| MBR | 135 | 3.562 | 1.779 | 1.218 | 12.074 |

| 25719 | 0.007 | 0.081 | 0 | 1 | |

| 25521 | 0.864 | 0.343 | 0 | 1 | |

| 25521 | 0.005 | 0.072 | 0 | 1 | |

| INDR | 31629 | 0.348 | 0.082 | 0 | 0.56 |

| Bsize | 31629 | 9.01 | 1.83 | 5 | 15 |

| edu | 24603 | 0.478 | 0.5 | 0 | 1 |

| tenure | 31322 | 7.379 | 4.576 | 1 | 17 |

| CEOpower | 31264 | 0.155 | 0.063 | 0.028 | 0.405 |

| CEOoverconfidence | 31347 | 12.302 | 2.17 | 0 | 14.88 |

| Pconnection | 31322 | 0.053 | 0.224 | 0 | 1 |

| magshare | 30464 | 0.097 | 0.175 | 0 | 0.679 |

| magsalary | 31629 | 14.646 | 0.928 | 12.136 | 16.808 |

| TOP1 | 31636 | 0.371 | 0.154 | 0.091 | 0.757 |

| lnasset | 31635 | 21.656 | 1.221 | 19.008 | 25.511 |

| Lev | 28250 | 0.463 | 0.203 | 0.07 | 0.972 |

| OCF | 28250 | 0.044 | 0.077 | 0.263 | |

| FirmGrowth | 28249 | 0.178 | 0.346 | 1.873 | |

| Age | 31730 | 14.271 | 5.709 | 3 | 29 |

| Listyear | 30344 | 9.413 | 6.042 | 1 | 24 |

Table 3 Group tests |

| All | pre-policy sample | post-policy sample | ||

| Variables | Mean | Mean | Mean | |

| Panel A: Corporate governance | ||||

| INDR | 0.348 | 0.251 | 0.366 | |

| Bsize | 9.01 | 9.675 | 8.881 | 28.590*** |

| edu | 0.478 | 0.357 | 0.501 | |

| tenure | 7.379 | 3.271 | 8.171 | |

| CEOpower | 0.155 | 0.143 | 0.157 | |

| CEOoverconfidence | 12.302 | 11.079 | 12.529 | |

| Pconnection | 0.053 | 0 | 0.063 | |

| magshare | 0.097 | 0.009 | 0.11 | |

| magsalary | 14.646 | 13.679 | 14.835 | |

| TOP1 | 0.371 | 0.431 | 0.359 | 31.051*** |

| Panel B: Corporate finance | ||||

| lnasset | 21.656 | 21.104 | 21.763 | |

| Lev | 0.463 | 0.471 | 0.461 | 3.332*** |

| OCF | 0.044 | 0.046 | 0.043 | 2.205** |

| FirmGrowth | 0.178 | 0.221 | 0.17 | 9.503*** |

| Age | 14.271 | 9.293 | 15.241 | |

| Listyear | 9.413 | 6.554 | 9.973 | |

| Panel C: M&A tendencies | ||||

| M&AC | 0.986 | 0.984 | 0.998 | 6.639*** |

| M&AA | 18.603 | 17.686 | 18.749 | |

| Panel D: M&A performance | ||||

| CAR | 0.001 | 0.003 | 0.002 | 0.071 |

| BHAR | ||||

| MBR | 3.562 | 2.778 | 3.815 | |

| Note: ***, **, and * represent coefficients that are significant at the 1%, 5%, and 10% levels, respectively. |

Table 4 OLS regression results |

| (1) | (2) | (3) | (4) | (5) | |

| Variables | M&AC | M&AA | CAR | BHAR | MBR |

| 0.446** | 5.679** | 0.842* | |||

| (0.012) | (0.049) | (0.089) | |||

| 0.791*** | |||||

| (0.004) | (0.061) | (0.545) | |||

| 1.349** | 0.713*** | 0 | 0.875 | ||

| (0.016) | (0.000) | (0.389) | (.) | (0.611) | |

| INDR | 0.632 | 0.308 | 1.519 | 3.954 | |

| (0.508) | (0.560) | (0.661) | (0.661) | (0.127) | |

| Bsize | 0.0274 | 0.0206 | 0.0952 | 0.086 | |

| (0.508) | (0.239) | (0.192) | (0.539) | (0.481) | |

| edu | 0.0498 | 0.130** | 0.204 | ||

| (0.608) | (0.017) | (0.501) | (0.643) | (0.351) | |

| tenure | 0.0780** | 0.00237 | 0.0111 | ||

| (0.028) | (0.913) | (0.931) | (0.824) | (0.990) | |

| CEOpower | 1.907*** | 0.583 | |||

| (0.039) | (0.000) | (0.474) | (0.852) | (0.747) | |

| CEOoverconfidence | 0.00474 | ||||

| (0.733) | (0.013) | (0.081) | (0.108) | (0.569) | |

| Pconnection | 0.142 | 4.608*** | |||

| (0.423) | (0.292) | (0.001) | (0.383) | (0.458) | |

| magshare | 0.492** | 7.838 | 2.755 | ||

| (0.049) | (0.546) | (0.351) | (0.742) | (0.531) | |

| magsalary | 0.182 | ||||

| (0.729) | (0.066) | (0.606) | (0.887) | (0.329) | |

| TOP1 | 0.554*** | 0.464 | 1.139 | ||

| (0.015) | (0.007) | (0.574) | (0.641) | (0.377) | |

| lnasset | 0.105* | 0.318*** | 0.274 | ||

| (0.057) | (0.000) | (0.096) | (0.411) | (0.012) | |

| Lev | 0.239 | 0.00697 | 5.685*** | ||

| (0.896) | (0.191) | (0.997) | (0.929) | (0.000) | |

| OCF | 0.153 | 0.0564*** | 2.24 | 6.724** | |

| (0.772) | (0.000) | (0.427) | (0.631) | (0.014) | |

| FirmGrowth | 0.0157 | 0.289 | 0.345 | ||

| (0.942) | (0.817) | (0.680) | (0.116) | (0.481) | |

| Age | 0.0193* | 0.0478 | 0.0406 | 0.072 | |

| (0.093) | (0.785) | (0.775) | (0.603) | (0.302) | |

| Listyear | 0.0123 | 0.033 | 0.0581 | ||

| (0.007) | (0.413) | (0.754) | (0.680) | (0.988) | |

| _cons | 11.33*** | 7.144** | 1.009 | 5.083 | |

| (0.020) | (0.000) | (0.027) | (0.856) | (0.203) | |

| Industry | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes |

| N | 225 | 6942 | 52 | 79 | 79 |

| adj. R2 | 0.183 | 0.138 | 0.589 | 0.315 | 0.553 |

| Note: Standard errors of regression coefficients are in parentheses. ***, **, and * represent coefficients that are significant at the 1%, 5%, and 10% levels, respectively. |

Table 5 Replacement of dependent variables |

| (1) | (2) | (1) | (2) | |||

| Variables | M&AD | CAR | Variables | M&AD | CAR | |

| magsalary | 0.00608 | |||||

| (0.009) | (0.309) | (0.012) | ||||

| 0.183 | TOP1 | |||||

| (0.106) | (0.213) | (0.047) | ||||

| 0.127*** | 0 | lnasset | 0.00262 | 0.0400** | ||

| (0.000) | (.) | (0.576) | (0.035) | |||

| INDR | Lev | 0.0682*** | ||||

| (0.389) | (0.825) | (0.002) | (0.368) | |||

| Bsize | 0.00865 | OCF | 0.00806*** | |||

| (0.008) | (0.438) | (0.000) | (0.183) | |||

| edu | 0.0151* | 0.0860* | FirmGrowth | 0.0475*** | 0.0479 | |

| (0.063) | (0.060) | (0.000) | (0.152) | |||

| tenure | 0.000204 | 0.0209** | Age | 0.00555 | ||

| (0.946) | (0.014) | (0.571) | (0.444) | |||

| CEOpower | 0.308 | Listyear | ||||

| (0.289) | (0.281) | (0.047) | (0.002) | |||

| CEOoverconfidence | 0.0018 | 0.000209 | _cons | 0.215** | ||

| (0.395) | (0.961) | (0.027) | (0.207) | |||

| Pconnection | 0.0374** | 0.143 | Industry | Yes | Yes | |

| (0.030) | (0.126) | Year | Yes | Yes | ||

| magshare | 0.121*** | 0.159 | N | 19938 | 73 | |

| (0.000) | (0.865) | adj. R2 | 0.029 | 0.486 |

| Note: Standard errors of regression coefficients are in parentheses. ***, **, and * represent coefficients that are significant at the 1%, 5%, and 10% levels, respectively. |

Table 6 Shortened time window |

| (1) | (2) | (3) | (4) | (5) | |

| Variables | M&AC | M&AA | CAR | BHAR | MBR |

| 0.490** | 6.387* | 0.853* | |||

| (0.012) | (0.052) | (0.082) | |||

| 0.888*** | |||||

| (0.005) | (0.061) | (0.549) | |||

| 0.993* | 0.293* | 0 | |||

| (0.067) | (0.085) | (0.773) | (0.515) | (.) | |

| INDR | 0.509 | 0.467 | 2.803 | 3.844 | |

| (0.702) | (0.412) | (0.489) | (0.324) | (0.199) | |

| Bsize | 0.00201 | 0.0238 | 0.136 | 0.0764 | |

| (0.969) | (0.220) | (0.217) | (0.371) | (0.557) | |

| edu | 0.0318 | 0.143** | 0.209 | ||

| (0.782) | (0.015) | (0.475) | (0.373) | (0.375) | |

| tenure | 0.0981** | 0.0116 | 0.0158 | 0.0328 | 0.0437 |

| (0.025) | (0.627) | (0.906) | (0.857) | (0.735) | |

| CEOpower | 1.932*** | 0.503 | |||

| (0.032) | (0.000) | (0.683) | (0.888) | (0.787) | |

| CEOoverconfidence | 0.00607 | ||||

| (0.640) | (0.031) | (0.065) | (0.175) | (0.925) | |

| Pconnection | 0.0342 | 4.669*** | |||

| (0.880) | (0.495) | (0.001) | (0.375) | (0.501) | |

| magshare | 0.560* | 8.69 | 0.83 | ||

| (0.093) | (0.216) | (0.324) | (0.922) | (0.807) | |

| magsalary | 0.0199 | 0.114 | 0.188 | ||

| (0.837) | (0.080) | (0.702) | (0.782) | (0.345) | |

| TOP1 | 0.467** | ||||

| (0.064) | (0.038) | (0.965) | (0.983) | (0.560) | |

| lnasset | 0.105* | 0.312*** | 0.415 | ||

| (0.082) | (0.000) | (0.157) | (0.157) | (0.012) | |

| Lev | 0.0758 | 5.546*** | |||

| (0.718) | (0.706) | (0.818) | (0.920) | (0.000) | |

| OCF | 0.115 | 0.0562*** | 2.131 | 6.803** | |

| (0.868) | 0.000 | (0.448) | (0.678) | (0.023) | |

| FirmGrowth | 0.0293 | 0.0989 | 0.141 | 0.307 | |

| (0.867) | (0.179) | (0.860) | (0.091) | (0.543) | |

| Age | 0.0183 | 0.0817 | 0.0572 | 0.0818 | |

| (0.150) | (0.736) | (0.638) | (0.407) | (0.281) | |

| Listyear | 0.0116 | 0.016 | |||

| (0.010) | (0.471) | (0.878) | (0.931) | (0.912) | |

| _cons | 11.94*** | 6.958* | 4.749 | ||

| (0.045) | (0.000) | (0.093) | (0.644) | (0.242) | |

| Industry | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes |

| N | 167 | 5765 | 50 | 74 | 75 |

| adj. R2 | 0.012 | 0.134 | 0.581 | 0.246 | 0.54 |

| Note: Standard errors of regression coefficients are in parentheses. ***, **, and * represent coefficients that are significant at the 1%, 5%, and 10% levels, respectively. |

Table 7 Heckman's two-stage results |

| (1) | (2) | (1) | (2) | |||

| Variables | First | Second | Variables | First | Second | |

| main | magshare | 0.346** | ||||

| 0.349*** | (0.001) | (0.036) | ||||

| (0.000) | Bsize | 0.0462* | ||||

| Tenderornot | 6.776*** | (0.073) | (0.129) | |||

| (0.001) | INDR | 1.041 | 0.315 | |||

| IMR | (0.250) | (0.527) | ||||

| (0.006) | OCF | 0.0661* | ||||

| CEOoverconfidence | (0.041) | (0.056) | ||||

| (0.917) | (0.000) | edu | 0.11 | 0.140*** | ||

| magsalary | 0.062 | (0.312) | (0.008) | |||

| (0.549) | (0.144) | tenure | 0.0966*** | |||

| TOP1 | 0.341 | 0.573*** | (0.024) | (0.000) | ||

| (0.345) | (0.002) | lnasset | 0.192*** | 0.312*** | ||

| Lev | 0.218 | (0.000) | (0.000) | |||

| (0.527) | (0.777) | CEOpower | 1.995*** | 1.635*** | ||

| FirmGrowth | 0.0269 | 0.0522 | (0.002) | (0.000) | ||

| (0.878) | (0.443) | Pconnection | ||||

| Age | 0.0341*** | (0.493) | (0.250) | |||

| (0.173) | (0.000) | _cons | 9.989*** | |||

| Listyear | 0.0453** | (0.000) | (0.000) | |||

| (0.018) | (0.001) | N | 6942 | 6942 | ||

| adj. R2 | 0.091 | |||||

| Pseudo R2 | 0.144 |

| Note: Standard errors of regression coefficients are in parentheses. ***, **, and * represent coefficients that are significant at the 1%, 5%, and 10% levels, respectively. |

Table 8 Moderating effect test results |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Variables | CAR1 | CAR2 | BHAR1 | BHAR2 | MBR1 | MBR2 |

| 0.0891*** | 0.181*** | |||||

| (0.009) | (0.000) | (0.674) | (0.001) | (0.528) | (0.382) | |

| 0.00443 | 4.656*** | 0 | 0.884 | 0 | ||

| (0.780) | (0.317) | (0.000) | (.) | (0.302) | (.) | |

| 0.240*** | 4.656*** | 0.953* | ||||

| (0.000) | (0.000) | (0.069) | ||||

| INDR | 0.0441 | 0.0445 | 9.143* | 7.213 | ||

| (0.605) | (0.526) | (0.654) | (0.654) | (0.056) | (0.124) | |

| Bsize | 0.00223 | 0.00165 | 0.279* | 0.256 | ||

| (0.467) | (0.512) | (0.966) | (0.966) | (0.072) | (0.149) | |

| edu | 0.709 | 0.709 | 0.414 | 0.226 | ||

| (0.407) | (0.054) | (0.259) | (0.259) | (0.490) | (0.630) | |

| tenure | 0.00025 | 0.0528 | 0.0753 | |||

| (0.247) | (0.940) | (0.498) | (0.498) | (0.730) | (0.542) | |

| CEOpower | 1.04 | 1.04 | ||||

| (0.405) | (0.197) | (0.681) | (0.681) | (0.724) | (0.605) | |

| CEOoverconfidence | ||||||

| (0.199) | (0.238) | (0.704) | (0.704) | (0.813) | (0.901) | |

| Pconnection | 0.142*** | 0.238*** | ||||

| (0.000) | (0.000) | (0.086) | (0.086) | (0.585) | (0.517) | |

| magshare | 0.207 | 0.0332 | 15.8 | 13.9 | ||

| (0.238) | (0.825) | (0.806) | (0.806) | (0.124) | (0.281) | |

| magsalary | 0.0153 | |||||

| (0.262) | (0.261) | (0.531) | (0.531) | (0.987) | (0.958) | |

| TOP1 | 0.0407 | 2.267 | 2.309 | |||

| (0.386) | (0.877) | (0.586) | (0.586) | (0.331) | (0.275) | |

| lnasset | 0.000109 | 0.0016 | 0.267 | 0.267 | ||

| (0.982) | (0.680) | (0.285) | (0.285) | (0.003) | (0.026) | |

| Lev | 0.00297 | 0.0221 | 0.374 | 0.374 | 8.793*** | 8.276*** |

| (0.942) | (0.517) | (0.819) | (0.819) | (0.000) | (0.000) | |

| OCF | 3.435 | 3.435 | 1.45 | |||

| (0.339) | (0.920) | (0.416) | (0.416) | (0.987) | (0.561) | |

| FirmGrowth | 0.41 | 0.352 | ||||

| (0.415) | (0.116) | (0.754) | (0.754) | (0.475) | (0.406) | |

| Age | 0.000812 | 0.00136 | 0.193** | 0.194 | ||

| (0.654) | (0.367) | (0.824) | (0.824) | (0.028) | (0.175) | |

| Listyear | 0.00248 | 0.0965 | 0.0965 | |||

| (0.331) | (0.872) | (0.429) | (0.429) | (0.474) | (0.216) | |

| _cons | 0.0157 | 7.062 | 8.057* | |||

| (0.891) | (0.252) | (0.113) | (0.546) | (0.126) | (0.082) | |

| N | 52 | 52 | 79 | 79 | 79 | 79 |

| adj. R2 | 0.314 | 0.535 | 0.341 | 0.341 | 0.526 | 0.574 |

| Note: Standard errors of regression coefficients are in parentheses. ***, **, and * represent coefficients that are significant at the 1%, 5%, and 10% levels, respectively. |

Table 9 Heterogeneity analysis results |

| Variables | M&AC | M&AA | M&AC | M&AA | |||||||

| SOE=1 | SOE=0 | SOE=1 | SOE=0 | large-scale | small-scale | large-scale | small-scale | ||||

| 0.610** | 1.051*** | 0.102 | 1.303*** | 1.184*** | 0.317 | ||||||

| (0.030) | (0.823) | (0.000) | (0.648) | (0.000) | (0.857) | (0.000) | (0.197) | ||||

| INDR | 0.0114 | 0.142 | 0.091 | 1.728 | 0.698 | ||||||

| (0.285) | (0.339) | (0.860) | (0.904) | (0.198) | (0.831) | (0.350) | (0.164) | ||||

| Bsize | 0.00088 | 0.037 | 0.0251 | 0.0214 | |||||||

| (0.211) | (0.170) | (0.889) | (0.205) | (0.732) | (0.106) | (0.356) | (0.384) | ||||

| edu | 0.0303 | 0.222** | 0.025 | 0.00123 | 0.141* | 0.102 | |||||

| (0.780) | (0.777) | (0.011) | (0.726) | (0.125) | (0.991) | (0.063) | (0.195) | ||||

| tenure | 0.00433 | 0.00021 | 0.035 | 0.0906* | 0.0259 | 0.0211 | |||||

| (0.911) | (0.913) | (0.323) | (0.253) | (0.061) | (0.543) | (0.371) | (0.518) | ||||

| CEOpower | 0.0914 | 0.971 | 2.191*** | 1.812*** | 1.971*** | ||||||

| (0.028) | (0.145) | (0.249) | (0.000) | (0.005) | (0.389) | (0.002) | (0.002) | ||||

| CEOoverconfidence | 0.00112 | 0.0242 | 0.0032 | ||||||||

| (0.941) | (0.074) | (0.009) | (0.447) | (0.490) | (0.857) | (0.047) | (0.086) | ||||

| Pconnection | 0.141 | 0.00522 | 0.039 | 1.080*** | |||||||

| (0.420) | (0.654) | (0.890) | (0.310) | (0.001) | (0.807) | (0.171) | (0.776) | ||||

| magshare | 0.405 | 0.014 | 0.157 | 0.426 | 0.692* | 0.00716 | |||||

| (0.144) | (0.612) | (0.875) | (0.561) | (0.427) | (0.060) | (0.195) | (0.975) | ||||

| magsalary | 0.0539 | 0.00037 | 0.012 | ||||||||

| (0.577) | (0.735) | (0.462) | (0.096) | (0.044) | (0.909) | (0.059) | (0.767) | ||||

| TOP1 | 0.710** | 0.447 | 0.625** | 0.259 | |||||||

| (0.023) | (0.428) | (0.045) | (0.101) | (0.548) | (0.166) | (0.028) | (0.386) | ||||

| lnasset | 0.136** | 0.446*** | 0.141*** | 0.346*** | 0.208** | 0.356*** | 0.122** | ||||

| (0.047) | (0.162) | (0.000) | (0.010) | (0.007) | (0.030) | (0.000) | (0.034) | ||||

| Lev | 0.202 | 0.012 | 0.334 | 0.239 | 0.625** | 0.126 | 0.410* | ||||

| (0.504) | (0.402) | (0.259) | (0.311) | (0.006) | (0.034) | (0.661) | (0.089) | ||||

| OCF | 0.171 | 0.042*** | 0.717 | ||||||||

| (0.815) | (0.512) | (0.112) | (0.001) | (0.657) | (0.273) | (0.124) | (0.213) | ||||

| FirmGrowth | 0.04 | 0.00163 | 0.067 | 0.497 | 0.0295 | 0.0966 | |||||

| (0.691) | (0.407) | (0.573) | (0.961) | (0.144) | (0.782) | (0.311) | (0.483) | ||||

| Age | 0.0163 | 0.056*** | 0.0158 | 0.0131 | |||||||

| (0.216) | (0.499) | (0.318) | (0.884) | (0.005) | (0.351) | (0.418) | (0.189) | ||||

| Listyear | 0.00061 | 0.022 | 0.012 | 0.0328 | 0.0098 | ||||||

| (0.574) | (0.743) | (0.329) | (0.594) | (0.012) | (0.648) | (0.103) | (0.665) | ||||

| _cons | 0.0407 | 9.036*** | 15.52*** | 11.06*** | 15.68*** | ||||||

| (0.458) | (0.275) | (0.000) | (0.000) | (0.085) | (0.287) | (0.000) | (0.000) | ||||

| Industry | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | |||

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | |||

| N | 166 | 3018 | 2765 | 4177 | 97 | 122 | 3470 | 3455 | |||

| adj. R2 | 0.062 | 0.024 | 0.18 | 0.12 | 0.153 | 0.084 | 0.168 | 0.113 | |||

| Note: Standard errors of regression coefficients are in parentheses. ***, **, and * represent coefficients that are significant at the 1%, 5%, and 10% levels, respectively. |

| 1 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 2 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 3 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 4 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 5 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 6 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 7 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 8 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 9 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 10 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 11 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 12 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 13 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 14 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 15 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 16 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 17 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 18 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 19 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 20 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 21 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 22 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 23 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 24 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 25 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 26 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 27 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 28 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 29 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 30 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 31 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 32 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 33 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 34 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| {{custom_ref.label}} |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

PDF(332 KB)

Table 1 Definitions of variablesTable 2 Descriptive statisticsTable 3 Group tests

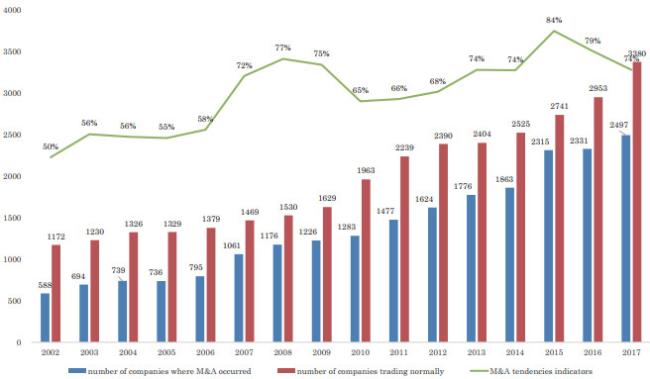

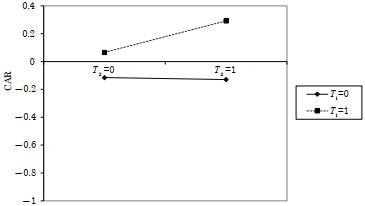

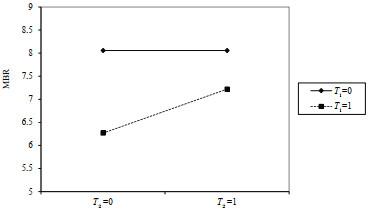

Table 1 Definitions of variablesTable 2 Descriptive statisticsTable 3 Group tests Figure 1 A-share listed companies' M&A tendencies during 2002–2017Figure 2 Number of M&A during 2002–2017Table 4 OLS regression resultsTable 5 Replacement of dependent variablesTable 6 Shortened time windowTable 7 Heckman's two-stage resultsTable 8 Moderating effect test resultsFigure 3 Moderating effect graph-CARFigure 4 Moderating effect graph-BHARFigure 5 Moderating effect graph-MBRTable 9 Heterogeneity analysis results

Figure 1 A-share listed companies' M&A tendencies during 2002–2017Figure 2 Number of M&A during 2002–2017Table 4 OLS regression resultsTable 5 Replacement of dependent variablesTable 6 Shortened time windowTable 7 Heckman's two-stage resultsTable 8 Moderating effect test resultsFigure 3 Moderating effect graph-CARFigure 4 Moderating effect graph-BHARFigure 5 Moderating effect graph-MBRTable 9 Heterogeneity analysis results/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}