PDF(171 KB)

PDF(171 KB)

Moving Average Model with an Alternative GARCH-Type Error

Huafeng ZHU, Xingfa ZHANG, Xin LIANG, Yuan LI

Journal of Systems Science and Information ›› 2018, Vol. 6 ›› Issue (2) : 165-177.

PDF(171 KB)

PDF(171 KB)

Moving Average Model with an Alternative GARCH-Type Error

Motivated by the double autoregressive model with order

moving average model / double autoregressive model / quasi maximum likelihood estimator {{custom_keyword}} /

Table 1 Bias and standard deviations of QMLEs |

| Bias | 0.0148 | 0.0038 | |||

| SD | 0.0229 | 0.0717 | 0.0614 | 0.0712 | |

| AD | 0.0179 | 0.0259 | 0.0481 | 0.0515 | |

| | Bias | 0.0077 | 0.0034 | ||

| | SD | 0.0155 | 0.0535 | 0.0462 | 0.0498 |

| AD | 0.0125 | 0.0213 | 0.0388 | 0.0412 | |

| | Bias | 0.0013 | 0.0243 | ||

| | SD | 0.0537 | 0.0739 | 0.0595 | 0.1082 |

| AD | 0.0548 | 0.0384 | 0.0556 | 0.0680 | |

| | Bias | 0.0011 | 0.0101 | 0.0006 | |

| | SD | 0.0384 | 0.0354 | 0.0390 | 0.0591 |

| AD | 0.0386 | 0.0321 | 0.0395 | 0.0629 | |

| | Bias | 0.0223 | |||

| | SD | 0.0678 | 0.1475 | 0.1108 | 0.0633 |

| AD | 0.0617 | 0.1239 | 0.1071 | 0.0495 | |

| | Bias | 0.0019 | 0.0105 | ||

| | SD | 0.0455 | 0.1078 | 0.0850 | 0.0491 |

| AD | 0.0462 | 0.0840 | 0.0820 | 0.0435 | |

| | Bias | 0.0018 | 0.0217 | ||

| | SD | 0.0385 | 0.1500 | 0.1055 | 0.0539 |

| AD | 0.0359 | 0.1345 | 0.0908 | 0.0400 | |

| Bias | 0.0048 | ||||

| SD | 0.0267 | 0.1020 | 0.0724 | 0.0363 | |

| AD | 0.0245 | 0.0897 | 0.0693 | 0.0204 |

| †Number of replications=1000. |

Table 2 Fitting performance for Models (8)–(9) |

| Model | RMSE for one-step-ahead forecast | Log-likelihood value |

| (8) | 0.0590 | 764.4363 |

| (9) | 0.0583 | 780.5071 |

| 1 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 2 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 3 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 4 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 5 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 6 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 7 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 8 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 9 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 10 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 11 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 12 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 13 |

Li G D, Zhu Q, Liu Z, et al. On mixture double autoregressive time series models. Journal of Business & Economic Statistics, 2015(in press).

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 14 |

Liu F, Li D, Kang X. Sample path properties of an explosive double autoregressive model. Econometric Reviews, 2016(in press).

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 15 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 16 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 17 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 18 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 19 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 20 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 21 |

Billingsley P. Probability and Measure. 3rd Edition, Wiley, New York, NY, USA, 1995.

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| {{custom_ref.label}} |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

The authors gratefully acknowledge the Editor and referees for their insightful comments and helpful suggestions that led to a marked improvement of the article.

PDF(171 KB)

Table 1 Bias and standard deviations of QMLEs

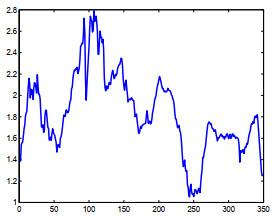

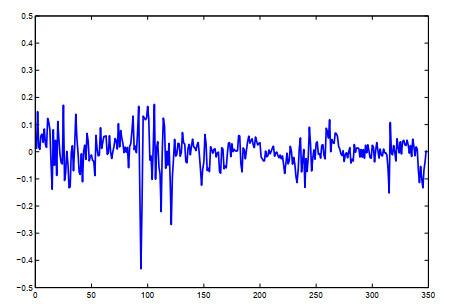

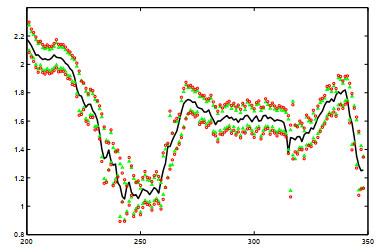

Table 1 Bias and standard deviations of QMLEs Figure 1 Time plot of Figure 2 Time plot of Table 2 Fitting performance for Models (8)–(9)Figure 3 Plot of the data

Figure 1 Time plot of Figure 2 Time plot of Table 2 Fitting performance for Models (8)–(9)Figure 3 Plot of the data /

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}