PDF(172 KB)

PDF(172 KB)

A KELM-Based Ensemble Learning Approach for Exchange Rate Forecasting

Yunjie WEI, Shaolong SUN, Kin Keung LAI, Ghulam ABBAS

Journal of Systems Science and Information ›› 2018, Vol. 6 ›› Issue (4) : 289-301.

PDF(172 KB)

PDF(172 KB)

A KELM-Based Ensemble Learning Approach for Exchange Rate Forecasting

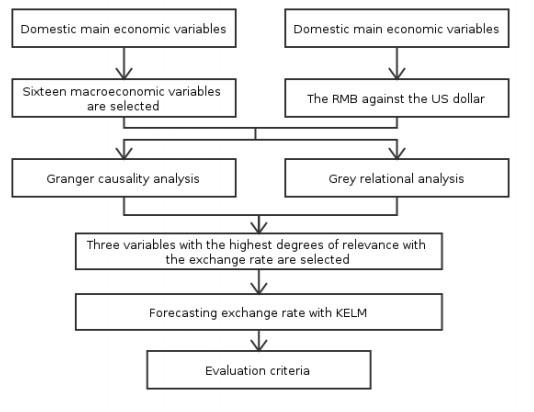

In this paper, a KELM-based ensemble learning approach, integrating Granger causality test, grey relational analysis and KELM (Kernel Extreme Learning Machine), is proposed for the exchange rate forecasting. The study uses a set of sixteen macroeconomic variables including, import, export, foreign exchange reserves, etc. Furthermore, the selected variables are ranked and then three of them, which have the highest degrees of relevance with the exchange rate, are filtered out by Granger causality test and the grey relational analysis, to represent the domestic situation. Then, based on the domestic situation, KELM is utilized for medium-term RMB/USD forecasting. The empirical results show that the proposed KELM-based ensemble learning approach outperforms all other benchmark models in different forecasting horizons, which implies that the KELM-based ensemble learning approach is a powerful learning approach for exchange rates forecasting.

exchange rate / macroeconomic variables / forecasting / kernel extreme learning machine {{custom_keyword}} /

Table 1 Statistical properties of the domestic economic variables and the exchange rate |

| Variable | Mean | Standard Deviation | Skewness | Kurtosis | Jarque-Bera | P value | Observations |

| RMB/USD | 6.40 | 0.25 | 0.60 | 2.15 | 7.75 | 0.02 | 85 |

| IM_LN | 7.28 | 0.13 | -0.82 | 3.91 | 12.45 | 0.00 | 85 |

| EX_LN | 7.46 | 0.16 | -1.28 | 5.09 | 38.87 | 0.00 | 85 |

| IM_YOY | 6.26 | 16.18 | 0.39 | 2.65 | 2.55 | 0.28 | 85 |

| EX_YOY | 7.46 | 13.77 | 0.43 | 3.40 | 3.20 | 0.20 | 85 |

| IPI | 100.77 | 8.94 | 0.21 | 1.98 | 4.32 | 0.12 | 85 |

| EPI | 101.87 | 4.46 | 0.63 | 2.43 | 6.71 | 0.03 | 85 |

| FER_LN | 10.42 | 0.11 | -0.21 | 2.76 | 0.84 | 0.66 | 85 |

| FER_YOY | 4.43 | 12.41 | 0.18 | 2.02 | 3.83 | 0.15 | 85 |

| CPI | 2.68 | 1.41 | 1.14 | 3.37 | 18.88 | 0.00 | 85 |

| PPI | 0.05 | 4.31 | 0.53 | 1.88 | 8.33 | 0.02 | 85 |

| RPI | 1.77 | 1.68 | 1.11 | 3.17 | 17.44 | 0.00 | 85 |

| M2_LN | 13.91 | 0.26 | -0.21 | 1.86 | 5.23 | 0.07 | 85 |

| M2_YOY | 13.54 | 2.25 | 0.76 | 3.83 | 10.65 | 0.00 | 85 |

| IVA | 9.13 | 3.49 | 0.68 | 3.62 | 7.95 | 0.02 | 85 |

| SZ_LN | 7.19 | 0.33 | 0.39 | 1.81 | 7.16 | 0.03 | 85 |

| SH_LN | 7.89 | 0.20 | 0.51 | 2.71 | 3.96 | 0.14 | 85 |

Table 2 Results of the Granger causality test |

| F-Statistic | Prob. | |

| IM_LN does not Granger Cause RMB/USD | 0.090 | 0.765 |

| RMB/USD does not Granger Cause IM_LN | 8.935 | 0.004*** |

| EX_LN does not Granger Cause RMB/USD | 5.416 | 0.023** |

| RMB/USD does not Granger Cause EX_LN | 4.389 | 0.040** |

| IM_YOY does not Granger Cause RMB/USD | 2.637 | 0.079 |

| RMB/USD does not Granger Cause IM_YOY | 5.009 | 0.009*** |

| EX_YOY does not Granger Cause RMB/USD | 14.491 | 0.000*** |

| RMB/USD does not Granger Cause EX_YOY | 1.154 | 0.286 |

| IPI does not Granger Cause RMB/USD | 1.140 | 0.349 |

| RMB/USD does not Granger Cause IPI | 4.256 | 0.002*** |

| EPI does not Granger Cause RMB/USD | 1.096 | 0.371 |

| RMB/USD does not Granger Cause EPI | 4.272 | 0.002*** |

| FER_LN does not Granger Cause RMB/USD | 5.976 | 0.017*** |

| RMB/USD does not Granger Cause FER_LN | 9.761 | 0.003*** |

| FER_YOY does not Granger Cause RMB/USD | 2.121 | 0.074 |

| RMB/USD does not Granger Cause FER_YOY | 1.855 | 0.115 |

| CPI does not Granger Cause RMB/USD | 2.888 | 0.062 |

| RMB/USD does not Granger Cause CPI | 6.684 | 0.002*** |

| PPI does not Granger Cause RMB/USD | 4.175 | 0.009*** |

| RMB/USD does not Granger Cause PPI | 5.122 | 0.003*** |

| RPI does not Granger Cause RMB/USD | 3.566 | 0.018*** |

| RMB/USD does not Granger Cause RPI | 4.044 | 0.010*** |

| M2_LN does not Granger Cause RMB/USD | 6.436 | 0.003*** |

| RMB/USD does not Granger Cause M2_LN | 0.064 | 0.939 |

| M2_YOY does not Granger Cause RMB/USD | 2.282 | 0.057 |

| RMB/USD does not Granger Cause M2_YOY | 0.507 | 0.770 |

| IVA does not Granger Cause RMB/USD | 4.531 | 0.006*** |

| RMB/USD does not Granger Cause IVA | 1.874 | 0.142 |

| SZ_LN does not Granger Cause RMB/USD | 7.051 | 0.000*** |

| RMB/USD does not Granger Cause SZ_LN | 3.678 | 0.016** |

| SH_LN does not Granger Cause RMB/USD | 3.442 | 0.021** |

| RMB/USD does not Granger Cause SH_LN | 2.750 | 0.049** |

| Notes: *** represent under 1% significant level ** represent under 5% significant level |

Table 3 Results of the grey relational analysis of RMB/USD and domestic economic variables |

| Variables | Correlation Degree | Variables | Correlation Degree |

| IM_LN | 0.775 | CPI | 0.711 |

| EX_LN | 0.726 | PPI | 0.535 |

| IM_YOY | 0.528 | RPI | 0.657 |

| EX_YOY | 0.524 | M2_LN | 0.771 |

| IPI | 0.648 | M2_YOY | 0.604 |

| EPI | 0.653 | IVA | 0.580 |

| FER_LN | 0.800 | SZ_LN | 0.813 |

| FER_YOY | 0.533 | SH_LN | 0.5815 |

Table 4 One-month-ahead forecasting results on monthly RMB/USD |

| Models | RW | ARIMA | VAR | LSSVR | KELM |

| MAPE (%) | 0.1920 | 0.3212 | 0.3277 | 0.2232 | 0.1515 |

| RMSE | 0.1319 | 0.2207 | 0.2252 | 0.1534 | 0.1041 |

Table 5 Three-month-ahead forecasting results on monthly RMB/USD |

| Models | RW | ARIMA | VAR | LSSVR | KELM |

| MAPE (%) | 0.4122 | 0.1736 | 0.2019 | 0.5301 | 0.1691 |

| RMSE | 0.3198 | 0.1454 | 0.1610 | 0.4038 | 0.1397 |

Table 6 Six-month-ahead forecasting results on monthly RMB/USD |

| Models | RW | ARIMA | VAR | LSSVR | KELM |

| MAPE (%) | 0.6574 | 0.6981 | 0.5917 | 0.5620 | 0.2236 |

| RMSE | 0.5686 | 0.6937 | 0.5508 | 0.4105 | 0.2098 |

| 1 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 2 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 3 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 4 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 5 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 6 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 7 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 8 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 9 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 10 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 11 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 12 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 13 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 14 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 15 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 16 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 17 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 18 |

Bhattacharya R, Patnaik H, Shah A. Monetary policy transmission in an emerging market setting. IMF Working Paper No. 11/5, International Monetary Fund, Washington D.C., 2011.

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 19 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 20 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 21 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 22 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 23 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 24 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 25 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 26 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 27 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 28 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 29 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 30 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 31 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 32 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 33 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 34 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 35 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 36 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 37 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 38 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 39 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| {{custom_ref.label}} |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

PDF(172 KB)

Figure 1 A KELM-based ensemble learning approach.

Figure 1 A KELM-based ensemble learning approach. Table 1 Statistical properties of the domestic economic variables and the exchange rateTable 2 Results of the Granger causality testTable 3 Results of the grey relational analysis of RMB/USD and domestic economic variablesTable 4 One-month-ahead forecasting results on monthly RMB/USDTable 5 Three-month-ahead forecasting results on monthly RMB/USDTable 6 Six-month-ahead forecasting results on monthly RMB/USD

Table 1 Statistical properties of the domestic economic variables and the exchange rateTable 2 Results of the Granger causality testTable 3 Results of the grey relational analysis of RMB/USD and domestic economic variablesTable 4 One-month-ahead forecasting results on monthly RMB/USDTable 5 Three-month-ahead forecasting results on monthly RMB/USDTable 6 Six-month-ahead forecasting results on monthly RMB/USD/

| 〈 |

|

〉 |

{kind=link}