1 Introduction

Numerus researches have indicated that the national real estate market of China has closely linked with the continuous strengthening of regional economic links and showed very strong systemic correlation, strengthening unceasingly along with the stimulation of a series of regulation and control measures

[1]. Driven by the interaction between policies and the promotion of urbanization, the linkage relationship between real estate market in various regions has become extensive and universal. Since 2015, "taking targeted policies to cut excess urban residential inventory" was established by central government to encourage local government take accurate regulation polices on its own market characteristics under the premise of "houses are used to live in, not to be used for speculation". However, since the implementation of the policies, large numbers of third-tier and fourth-tier cities still closely follow the market changing of adjacent first-tier and second-tier cities, making their local policies ineffective. Such regional interference had seriously disturbed the original intention of policy principle "one city, one strategy" and indicated the regulation process and policy effect of real estate in various regions will not only depend on their own transmission factors, but also are interfered by others through the spatial linkage relationships.

The spatial stickiness (defined as time connectivity, correlation and attractiveness between industries within a specific space) among different real estate sub-markets may result in the house market changing in central areas which can spill to adjacent areas and cause drastic market fluctuations. This conduction has certain attenuation in the time dimension, and unidirectional characteristic in the spatial dimension which was manifested as the ripple effect in space and time

[2-5] supported by immense amounts of empirical researches at transnational and national levels. For example, it was founded that UK had certain spillover effect of housing price to surrounding cities

[6] and London even had transnational spillover correlation with New York

[7], this effect also existed in the US real estate market

[8-10], New Zealand

[11], Finland

[12] and Australian

[13]. Lots of localization researches verified the significant diffusion effect of housing price among regions in China

[14-17]. Therefore, there is an interrelated feature of spatial and time stickiness between distinct but geographically adjacent real estate sub-markets. As the real estate regulation and control policies are important factors affecting the real estate market fluctuation, they will have initial impacts on important real estate economic system and conduct comprehensive transmission to various regions of the real estate system through the spatial linkage of the market. The spillover effect may distort the regulation effect in the transmission process, making the regulation policies of each sub-market interfere with each other

[18, 19]. Base on this, the first hypothesis is proposed as follows:

H1 When the housing transactions of central cities have strong political and economic influences affected by its local regulatory policies, the market fluctuations will spill over into the peripheral cities synchronously or laggingly, meanwhile, the influenced cities feedback with relatively weaker impacts which are insufficient to cause volatility of central cities' market, this unidirectional diffusion tends to form ripples in dimensions of time and space.

It is noticeable that although the central cities' policy may have certain regional spillover effect, some significant policies tended to effect in the form of information dissemination

[20, 21], the geographically distant regions also tend to take them as indicators and show strong market resonant in the circumstances of space variable that can be relatively ignored. Therefore, the second hypothesis is:

H2 Some important urban regulation policies, especially policies with strong political and economic signals, may overcome the limitations of geographical factors and produce "cross-regional" spillover effect on the whole national housing market.

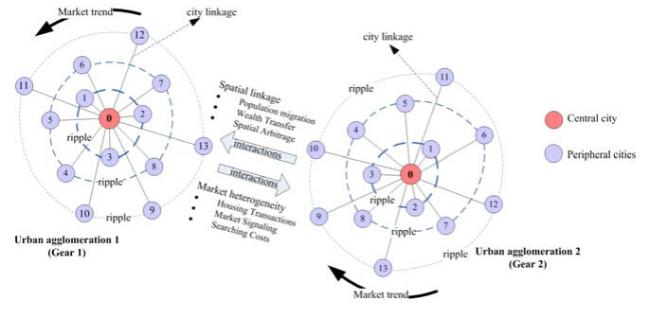

The immobility and the regionality of real estate product consumption make the development of real estate industry have obvious regional characteristics in a country which has vast territory as China. The level of economic development, customs and natural resource characteristics of a region determined the supply and demand characteristics of the regional housing market. The significant differences in regional financial frictions, industrial structure and other economic factors have resulted in different transmission effects of national or local regulatory policies in different regions of China in the past dozen years. Reasons of population migration, wealth transfer, spatial arbitrage, housing transaction, market signaling and search cost among regions made adjacent regional real estate market closely correlated

[22, 23] which has been supported by vast local studies and provided empirical evidence for the implementation of differentiated regulatory policies in China. Such correlation can be that adjacent regions develop in the same direction based on complementary advantages, or that different directions occur in the mutual absorption and competition for population and resources. This co-direction or non-direction running relationship is extremely similar to "gear transmission". Suppose that use the gear running structure to express the linkage effect between regions, as shown in

Figure 1.

Figure 1 Market radiation and geared interactions in adjacent regions |

Full size|PPT slide

The central cities marked with 0, while the rest were the peripheral radiation cities . The change of the housing market in the central city will have a certain spillover effect on the peripheral cities in time and space, which is manifested as a certain urban agglomeration. There may be some interaction ways between two adjacent markets, on the one hand, industrial development, policy intervention, population overflow and other factors may drive same market changing direction of two adjacent region; on the other hand, the mutual absorption of population and resources between adjacent economic regions which leads to reversely developing direction of the two sub-markets. Therefore, the third hypothesis is put forward as:

H3 Due to the mobility of population, information and resources, adjacent agglomeration housing markets radiating by the different central cities may have certain interactions.

To verify the above hypotheses, 156 prefecture-level cities' housing transaction data and 167 urban housing regulation policies promulgated by 10 central cities between January, 2010 and December, 2018 which were chosen as samples in our study, by integrating spatio-temporal model and event analysis method, compiled by MATLAB R 2015b, the three-dimensional wave of policy spillover from central cities to peripheral cities and the market interaction between different regions driven by policies in China's local housing market were simulated. This research intends to focus on questions of: what kind of spillover effect can the regulation policies of some central cities have on the housing market of peripheral cities and what are the interrelated effects of regional housing markets in the form of urban agglomeration under the condition of policy intervention.

The contributions of this study to the literature are in the following aspects: Firstly, this is an attempt to investigate the spatio-temporal housing market spillover effect in the perspective of urban policy intervention, which is an expansion of the housing price spillover studies in the vivid policies which oriented Chinese housing market. Since most of the current studies focus on the house price spillover from systemically important cities to the peripheral cities based on different sample sizes, few studies start from the regional perspective of local urban real estate policies to discuss the heterogeneous responses and interrelated ways of regional housing markets under such regulatory policy interventions. This study took a larger sample of cities than the current largest sample of 70 large and medium-sized cities in China

[17] as research objects and introduced the quantified policies into the spatio-temporal, to avoid the limitation of time and space variables which tend to be unusable at the same time in traditional economic quantitative methods and intuitively showed the regional and cross-regional spillover effects of policy shocks in the a spatiotemporal perspective.

Secondly, this work try to describe the policy-driven interactions of the housing market in adjacent regions based on urban agglomeration scope, which represents the main concentrated conomic strucutrues in China. In a huge market with regional heterogeneity, the interactions between different sub-housing markets may represent the flowing directions of economic factors

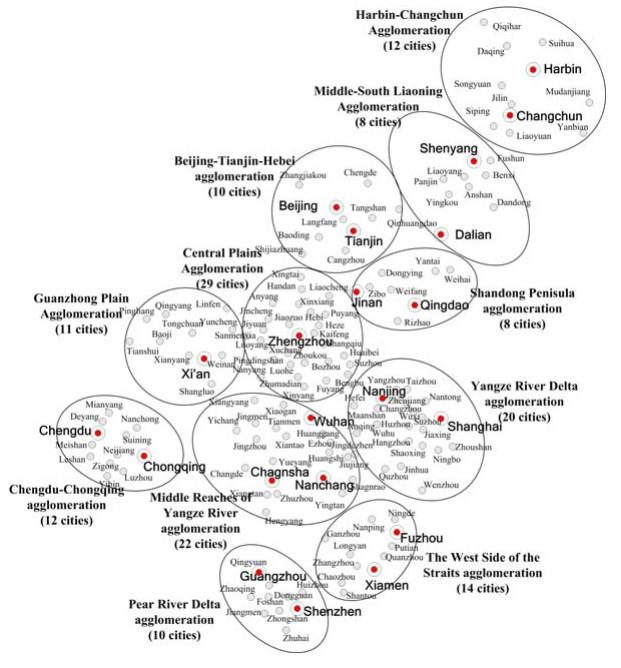

[24, 25]. The previous researches on the division of regional real estate market were often based on the roughly east coast, central and western inland zones, however we divide the regional market in a more nuanced and practical way of urban agglomerations. By using the unprecedented houing data of 156 prefecture level cities and 167 items of policies, this paper studied the interactions of 11 main economic zones of Harbin-Changchun agglomeration, Middle-South Liaoning agglomeration, Beijing-Tianjin-Hebei agglomeration, Shandong Peninsula agglomeration, Central Plains agglomeration, Guanzhong Plain agglomeration, Middle Reaches of the Yangtze River Agglomeration agglomeration, Yangtze River Delta agglomeration, Pearl River Delta Aagglomeration, West Side of the Straits agglomeration, Chengdu-Chongqing agglomeration under the policy regulation driven of the important cities Shenyang, Beijing, Qingdao, Zhengzhou, Xi'an, Wuhan, Shanghai, Shenzhen, Xiamen and Chongqing respectively. The results help to understand the regional linkage and policy transition mechanism in China's housing market.

Finally, extend the studies of regional housing spillover effect from new perspective of the fluctuation housing transaction rather than housing price. Since the housing price spillover effect widely existed in the Chinese real estate market which virified by a large number of empirical studies, this work turned to use the more market-sensitive transaction data to explore the spillover effects in the regional housing market. On the one hand, the transaction data contains more fluctuation details, which makes the policy shock quantification implementable by event analysis method

[21]. On the other hand, besides a strong correlation with house prices

[26, 27], the housing transaction tends to be more likely to reflect consumer's real attitude towards market changes than housing price

[28, 29]. The spillover effect based on the housing transaction volatility enriches the theory of region real estate.

2 Data

Since the basic mode of urban space development and main form of China's future economic development are urban agglomerations with different level cities organized by regional grids and guided by a few central cities with strong political and economic radiating capacities, therefore the housing sub-markets were divided by urban agglomerations. Based on the database of China Real Estate Index System (CREIS), 156 prefecture-level cities house market in 11 major urban agglomerations were chosen as research samples, as shown in Figure 2.

Figure 2 City samples in urban agglomerations |

Full size|PPT slide

Most existing researches on the spillover effect of real estate were basically based on the diffusion of housing price from important cities to surroundings. However, this study focus on the temporal and spatial diffusion wave generated by the regulation policies, so the quantification of the policy shock is of vital importance. During the past decade, there was a trend of single inflation of prices in China's housing market and lacking fluctuation information, which is essential to reflect the traces of policy impacts. In view of the sensitivity of housing transaction information to policy

[30, 31], transaction data are used to simulate the impact of policy instead of housing price data in this study.

To ensure data availability and integrality, the commodity residential housing transaction data of the 156 prefecture-level cities between January 2010 and December 2018 was selected as study samples. Removing the seasonal factors, all data were logarithmically processed before entering into the spatial-temporal model. Generally, an agglomeration may contain several big cities with strong political and economic influence, however, being limited to the model setting and the empirical facts that important cities with severe market conditions could significantly affect the market fluctuation of surrounding cities

[9, 16], this study just choose Changchun, Shenyang, Beijing, Qingdao, Zhengzhou, Xi'an, Wuhan, Shanghai, Chongqing, Xiamen and Shenzhen as the central cities in each agglomeration to study their policy spillover and the impacts on the regional housing market.

Another important consideration is the choice of urban policies. In order to simulate the policy spillover effect by central cities, it is necessary to eliminate the interference of central government policies and local policies of peripheral cities, therefore, we made detailed inspection by analyzing the cumulative abnormal fluctuations before and after the national and local policies promulgated to estimate their impacts on market volatility, with noisy policies, using the estimated window average value to substitute the abnormal value so as to filter out the influence of national policies and peripheral cities' policies (method in Subsection 3.2). The sample central cities' policies promulgated between January, 2010 and December, 2018 were selected as text samples. There are several basic principles to filter policies: Firstly, policies promulgated by local government or its directly affiliated departments; secondly, direct regulation and control policies on the real estate market that significantly affect market volatilities (verification see Subsection 3.2); thirdly, the policies contents can directly reflect the government's regulation willingness. The distribution of policy samples after sorting is: Shenyang 16 items, Wuhan 15 items, Shanghai 17 items, Beijing 16 items, Shenzhen 18 items, Xi'an 12 items, Chongqing 18 items, Qingdao 16 items, Zhengzhou 21 items and Xiamen 18 items.

3 Methodology

The basic idea of this study is to explore the spillover mechanism of quantified policies issued by central cities through linkages between cities within and outside the urban agglomeration scope. Therefore, we mainly establish the linkage between the housing market of central cities and peripheral cities with the spatio-temporal model, and the event analysis method is used to quantify the policy impacts. Here firstly outline the spatio-temporal model, then following with event analysis.

3.1 Spatio-Temporal Model

The most widely used method to study the correlation between policy variable and market volatility is vector auto regression (VAR) which is a conventional method to study the ripple effects of house price from central cities to surroundings based on assumption that time and space variables are unable to be simultaneously changed, so generally we only get the information in time dimension. Then spatio-temporal VAR technique as complement tools began to be used on the interconnections between house movements across cities over time as well as space

[3], it was so effective that being widely used to illustrate the house market linkage between cities across regions. Many investigations support that it can better illustrate dynamics characteristics between real estate markets in the time and space than the traditional non-spatial methods

[6, 7, 9, 10]. This model was set by referring to Holly's spatio-temporal model, which basic processes are as below:

Suppose there is cities marked with () and one central city marked with 0 in agglomeration , is the housing transaction value of city at time , which is influenced by its historical changing and other linked cities' market fluctuation in . When central city promulgated certain regulation policies (policy shock) which caused local market volatility, the marginal transaction level and its radiation peripheral cities' marginal trading are:

where

is the coefficient of deviation between central city and other cities;

is the quantized policy impact variable;

represents the spatial matrix of city

which is calculated by geospatial weight

[7, 32]. The common geospatial weight was calculated by using the straight-line distance between city

and

divided by the sum

[16]. However, we use shortest traffic distance

which is more persuasive and practical in the people's consideration of the housing location choice. The spatial factors conditions are as follows:

To make sure policy shock did caused by central city and spillover to other cities in agglomeration , the radiation cities' policy variables were ignored and we let . The marginal transaction changing of city caused by central city 0 will be:

To be more specifically, it can be adjusted to

The assumption of marginal level of

caused by policy shockb

which is exogenous variable that could be verified by Wu's program

[33] and Hausman's category test

[34]. Since the geospatial weight coefficients matrix was standardized as

and

is rank-deficient, the marginal transaction could be expressed as:

where , , and . is nonsingular matrix, and has same deficit rank. Let , and are matrixes. The function is

where and which could illustrate the time dependence between cities and reflecting spatial association. The generalized impulse response function of a unit under the level is

where is the information at , is one unit pulse of the policy shock, , let the initial setting is . The continuous response function is

Based on this, the function of central city's policy shock on the housing transaction change is established.

3.2 Event Analysis

From the spatio-temporal function of Equation (9), the quantization of policy shock

and

which are commonly regarded as stochastic factors is of great importance. Therefore, event analysis

[35], a widely used method in studing the impact of critical events on prices and trading volatility in finance market is introduced. The basic idea of the method is to test and estimate the influence of critical events on economic data changing by comparing and verifying the accumulative fluctuation of data before and after the events. The basic operating steps are:

Suppose is the trading value of original sequence, to keep time series stationary, processing it with first-order logarithmic transaction:

For the policy , let time as the initial impact time, set certain trading time units before and after the policy event as the corresponding "estimate window" and "test window". The policy shock at time is

According to the test window, for time , the test window could be divided into a pre-event test window by extracting trading time units before event time and a post-event test window after trading time units of the event time. The two sets are independent of each other and follow a normal distribution, for the unknown fuzzy policy point, assume it did not make any market abnormal volatilities, then let

The joint density probability function of the two types windows could be made as:

and are independent of each other and subject to the distribution. Let the follows the distribution, the assumption is denied at the situation of or which prove that the policy did have an effect. When , the policy shock is positive and is the negative. Taking certain significance level , the policy shock can be estimated. For the continuous effect of policy shock, assuming that the initial policy impact does not cause any fluctuations, test is carried out and rejecting condition of initial hypothesis is found by expanding the test window . In this, the policy variable is quantized and introduced into the saptio-temporal model.

4 Empirical Processes

This study conducted empirical analysis on the housing transaction data of 156 cities as samples. Firstly, the spillover effects of 167 regulation policies in 10 central cities within the scope of urban agglomeration is explored, including parameter estimation, spatial-temporal ripple simulation and policy analysis. Then we adjust the geospatial variable and study the cross-regional spillover effect in the situation of predefined region settings, mainly including parameter estimation and cross-regional spatio-temporal ripple simulation. Finally, the overall regional housing markets are taken as the research objects to explore the interactive structures.

4.1 Regional Policy Spillover Effect

Firstly, unit root test was carried out on the 156 cities' data, and it was founded that except city Changchun in Harbin-Changchun agglomeration, all the other 10 central cities had unit roots and met the requirements of the model. In view of the Harbin-Changchun agglomeration and Middle-south Liaoning agglomeration are geographically close, I combined the two and explored city Shenyang's policy influence on the cities of these two agglomerations. In view of Beijing's special political and economic status, it was found that Yingkou and Dalian in Middle-South Liaoning Agglomeration, Jinan, Weifang and Dongying in Shandong Peninsula agglomeration were more affected by Beijing than Shenyang and Qingdao respectively, thus I appropriately expanded the scope of Beijing's influence.

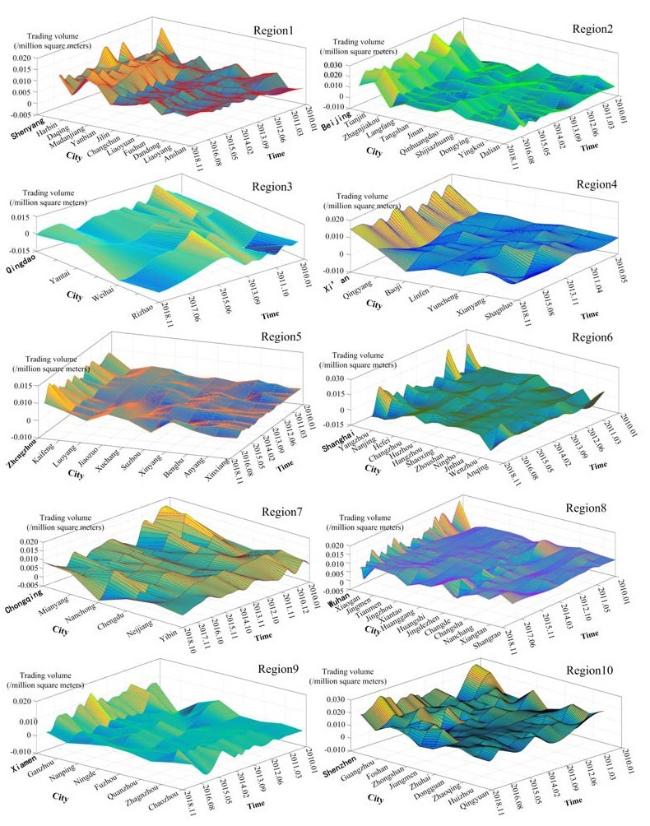

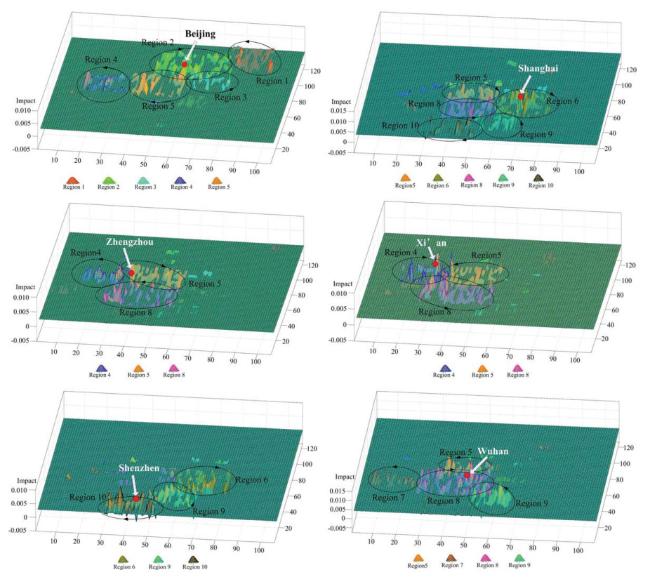

Based on the above model proposed in Subsection 3.1, the spatio-temporal linkage models were established according to the transaction data of 156 cities. The spatial variable was weighted by the shortest traffic distance between city 0 and city and the regional linkage equation used the least squares estimator for regression analysis. Removing the cities with insignificant regression coefficient, 105 cities in 10 regions were entered into the model. For intuitively visualizing the spillover "ripple" caused by central cities' policies, continuously generalizing impulse response functions of the central cities' regulation policies were constructed by integrating spatio-temporal model and event analysis, the spatial and temporal ripple in different regions were simulated through MATLAB R2015b, the 3 dimensional diagrams are shown in Figure 3.

Figure 3 Spatial and temporal ripples of the regional housing market |

Full size|PPT slide

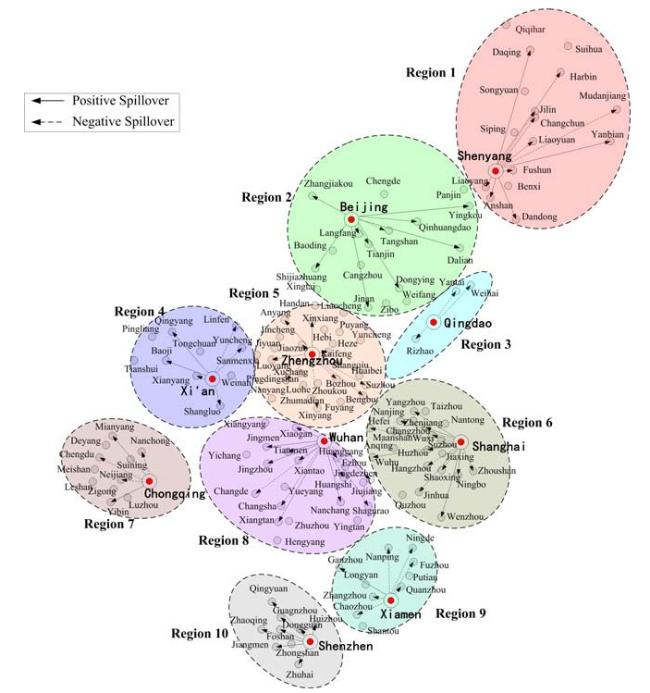

It can be seen that the 10 central cities have obviously caused the changes of the housing market in related cities, which is manifested as the significant space-time ripple effect and the spillover effect of the policy varies according to the heterogeneous regional characteristics of the housing market. Graphically the spillover effect is more noticeable in Region 1, Region 7, Region 9 and Region 10 which embodied in the central city's regulation policies causing large volatility in its own housing transaction and having larger wave hits on the radiation surrounding cities. Conversely the policy spillover in Region 2, Region3, Region 4, Region 5, Region 6, Region 8 are relatively modest, performing as the housing transactions are less affected by the central city's policies and cause smaller wave hit to the radiation peripheral cities. Combining with the above research results, geographical indications of the central cities' policy spillover direction and scope in each region was made, with solid lines represent positive spread, the dotted line represents the negative and finally got the spillover direction diagram, as shown in Figure 4.

Figure 4 The spillover directions of central city's policies in the adjusted regions |

Full size|PPT slide

The above figure reflects the geographical distribution of 10 central cities' real estate policy influence in each region which reflects the core driving force of the central city in China's regional housing market. Specifically, although Shenyang is not the central city in Harbin-Changchun agglomeration but it did has significantly impacts on the whole north-east area; The regional spillover effect of Beijing's policy was unexpected, although Beijing has a wide range of influence, it did not have a large impact on the cities in the Beijing-Tianjin-Hebei urban agglomeration for the spillover ripple was not large with the small coefficient of difference, however it had a relatively larger impact on cities in Liaoning province (Dalian, Yingkou) and Shandong province (Jinan, Dongying); The policy spillover effect of Qingdao was only effective in Jiaodong Peninsula, this may on account of Qingdao is not the provincial capital, however the spillover effect was not obvious by the capital city Jinan in our study neither; The policies of Xi'an had significant impacts on 6 cities in Region 4 with small wave hits; Zhengzhou had impacts on 9 cities, a very low proportion in Region 5 and low spillover force from the perspective of ripple shape, indicating that Zhengzhou did not have so extensive policy influence of real estate in Central Plain area; Shanghai's policy spillover effect had significantly large scope, it was obvious that the policy shock would spread to the surrounding areas, especially to the southern cities, besides geographical proximity, close economic ties may be one of the important reasons, however the impact was relatively modest judging from the spatial and temporal ripple; Chongqing's policy spillover only affected 5 cities in Region 7, but it caused large fluctuation in the market and had certain substitution with another important city Chengdu in Region 7; The spillover effect of Wuhan's policy was very significant, 13 cities in the Region8 had been affected, except for Changsha, Shangrao and Changde showed certain competition relation, the rest of the cities had positive relationships with Wuhan; Xiamen also showed a strong spillover effect in Region 9 but it had obvious substitution effect with most of the significantly correlated cities such as Fuzhou, Ningde, Ganzhou and Chaozhou; Shenzhen's policy impact on the Region 10 was very obvious, which were basically positive, and even had a significant positive impact on Guangzhou, but did not show obvious substitution effect between the two.

In order to make clear of the mechanism of different policy types, the spillover effect producing by each regulation policy was verified item by item. Firstly let the quantized sample policies enter into the integrated model one by one, the abnormal volatilities were simultaneously identified in impacting amplitudes and effecting time, then the effective policy item was identified by backstepping O-Lag time units. Finally the policies with wide influence scope and long effect time were sorted out and shown in Table 1.

Table 1 Policies with strong cross-regional spillover effects |

| Issued time | Major policy items | O-Lag/month | Effect time/month | Effect range/cities |

| | Shenyang (Region 1) | | | |

| Aug., 2014 | Purchase restrictions relaxation | 0.2 | 3 | 8 |

| Nov., 2014 | Accelerate rebuild shanty towns | 0.3 | 4 | 8 |

| Feb., 2015 | Compensation for house expropriation | 0.3 | 3 | 10 |

| Dec., 2016 | Speed up reduce unsold houses | 0.4 | 6 | 7 |

| | Beijing (Region 2) | | | |

| Apr., 2010 | Curb excessive house price rises | 0.1 | 2 | 11 |

| Feb., 2011 | Beijing 15 macro control policies | 0.2 | 2 | 8 |

| Oct., 2013 | Purchase limitation supervision | 0.1 | 1 | 7 |

| Mar., 2017 | Diversified housing credit policies | 0.3 | 2 | 9 |

| | Xi'an (Region 4) | | | |

| Feb., 2011 | Purchase restrictions | 0.3 | 1 | 6 |

| Jun., 2016 | Measures to reduce unsold houses | 0.8 | 9 | 6 |

| Apr., 2018 | Housing policy for talent introduction | 0.6 | 5 | 5 |

| | Zhengzhou (Region 5) | | | |

| May, 2014 | Portfolio loan of accumulation fund | 0.2 | 2 | 9 |

| Feb., 2016 | Adjustment of tax | 0.3 | 1 | 9 |

| Oct., 2016 | Housing purchase restriction policy | 0.2 | 1 | 10 |

| | Shanghai (Region 6) | | | |

| Jan., 2011 | Details of limited purchasing order | 0.2 | 12 | 12 |

| Nov., 2016 | Diversified housing credit policies | 0.2 | 4 | 11 |

| | Chongqing (Region 7) | | | |

| Sep., 2014 | Housing property tax collection | 0.3 | 2 | 5 |

| Oct., 2015 | Accelerate rebuild shanty towns | 0.1 | 6 | 6 |

| Jan., 2017 | Housing property tax collection | 0.1 | 2 | 5 |

| | Wuhan (Region 8) | | | |

| Jan., 2011 | Limited purchasing order | 2.8 | 4 | 10 |

| Dec., 2013 | Public accumulation funds | 0.2 | 3 | 10 |

| Sep., 2015 | New provident fund loan details | 0.7 | 4 | 11 |

| Nov., 2015 | Housing accumulation fund loan | 1 | 3 | 8 |

| Mar., 2016 | Accelerate rebuild shanty towns | 0.8 | 1 | 7 |

| Oct., 2016 | Restriction on purchase and loans | 0.3 | 2 | 8 |

| | Xiamen (Region 9) | | | |

| Nov., 2014 | House purchase and credit limitation | 3.1 | 5 | 7 |

| Jan., 2016 | Monetary compensation | 0.8 | 4 | 6 |

| Nov., 2016 | Registration of real estate | 2.6 | 2 | 8 |

| Oct., 2017 | Rebuild shanty towns | 1 | 5 | 7 |

| | Shenzhen (Region 10) | | | |

| Sep., 2010 | Curb house price rises | 0.2 | 11 | 8 |

| Oct., 2013 | Stable housing prices | 0.2 | 10 | 7 |

| Mar., 2016 | Improve security system | 0.2 | 12 | 5 |

It is founded that the spillover effects of real estate policies in different regions both had commonnesses and distinct regional characteristics. For the first-tier cities of Beijing, Shanghai and Shenzhen, the restrictive policies, specifically the administrative order policies of Beijing, procurement and loan limit policies of Shanghai and Shenzhen, had strong spillover effects in wide space scope but short duration in time. However, in addition to restrictive policies, the shanty town reconstruction type policies especially monetization compensation policies of second-tier cities, as Shenyang, Xi'an, Zhengzhou, Chongqing, Wuhan and Xiamen had significant spillover effects.

As for regional characteristics, Shenyang's policy of stimulating consumption had a great influence on Northeast China. The talent settlement policy and reducing unsold houses policies in Xi'an had relatively long impact on the Guanzhong Plain region. Zhengzhou's provident fund policy and transaction tax policy had extensive influence but short lived on the Central Plains. Chongqing's real estate tax policies had certain spillover effect, this related to its identity of one of the pilot cities of China's real estate tax. Wuhan had longer effect lag and more strong spillover effect policies, among which provident fund policies exerted more extensive impacts than other central cities. Xiamen's real estate registration policy had certain spillover effects on the West Side of the Straits agglomeration, which may indirectly reflect higher level of property speculation in this region.

4.2 Cross-Regional Policy Spillover Effect

Through the above research that the important cities' real estate policies have certain regional spillover characteristics, however, some special important regulation policies actually tend to spread in the form of information dissemination rather than geographical factors, which behaves as geographical remote cities also tend to take them as indicators, that is these policies can not only spill in certain region, but also have cross-regional action. In addition, due to the impact of family migration, wealth transfer, space arbitrage, housing transactions and search costs, there must be some interactions between the real estate markets in different regions

[22, 23]. Therefore, this part focuses on two questions of to what extent central city's policies caused cross-regional market interaction and what were the interactions between regional housing markets driven by the policies of central cities.

This section studies the spillover effects of the central cities on each city and each region. Firstly, the spatial variable matrix was adjusted to the unit matrix and the spatiotemporal models of 10 central cities with all the sample cities were constructed respectively, the spillover situation of the regulation policies of different central cities without geographical space restrictions was analyzed. Secondly, We explored the spillover effect of the central city on the whole of different regions. The total transaction data of the remaining cities (excluding the central cities) were taken as the overall market transaction data of the region. Removing seasonal factors and the natural logarithm was taken into the model, the calculation results showed that the overall data of the 10 regions were all stationary sequences and all have unit roots. The change of housing market in each region is regressive by its lag term and the equation of each region is estimated by the least square method. The spatio-temporal model is established with each central city as the policy impact point, by combining the significance of regional deviation coefficient, lag term coefficient statistics and Wu-Hausman statistical test, the models with significant regression results were selected and the estimated results of the model are shown in Table 2.

Table 2 The properties of defined cases used for simulating of spontaneous imbibition process |

| Linked Regions | Linked cities | | | O-Lag | N-Lag | Cnt | W-H T |

| Beijing | | | | | | | |

| Region 1 | 10 | 0.143** | 0.108** | 0.011 | 0.013 | 0.105** | 0.043 |

| | | (2.333) | (0.546) | (0.780) | (0.654) | (1.900) | |

| Region 3 | 3 | 0.109** | 0.142** | 0.013 | 0.046 | 0.107** | 0.055 |

| | | (2.443) | (2.058) | (0.475) | (0.532) | (2.011) | |

| Region 4 | 4 | 0.093 | 0.108** | 0.100 | 0.006 | 0.009 | 0.045 |

| | | (3.065) | (2.017) | (2.209) | (0.039) | (0.055) | |

| Region 5 | 14 | 0.032* | 0.456*** | 0.162*** | 0.009 | 0.122** | 0.093 |

| | | (1.771) | (3.990) | (3.220) | (0.300) | (2.421) | |

| Zhengzhou | | | | | | | |

| Region4 | 6 | 0.124** | 0.023 | 0.109** | 0.082* | 0.032* | 0.068 |

| | | (1.871) | (0.946) | (2.487) | (1.755) | (1.673) | |

| Region8 | 8 | 0.188** | 0.077 | 0.345*** | 0.398*** | 0.039* | 0.109 |

| | | (1.701) | (1.425) | (3.988) | (4.760) | (1.703) | |

| Shanghai | | | | | | | |

| Region5 | 5 | 0.061 | 0.120** | 0.109** | 0.276*** | 0.084* | 0.075 |

| | | (2.303) | (2.330) | (2.390) | (3.394) | (1.734) | |

| Region8 | 12 | 0.133** | 0.106** | 0.089** | 0.211*** | 0.055* | 0.044 |

| | | (2.000) | (2.031) | (2.240) | (3.678) | (1.709) | |

| Region9 | 9 | 0.120** | 0.100** | 0.134** | 0.194*** | 0.098** | 0.190 |

| | | (2.069) | (2.109) | (2.553) | (3.098) | (2.111) | |

| Region10 | 5 | 0.007 | 0.543*** | 0.345*** | 0.220*** | 0.058* | 0.300 |

| | | (2.448) | (5.567) | (3.507) | (4.222) | (1.688) | |

| Wuhan | | | | | | | |

| Region5 | 8 | 0.146*** | 0.024 | 0.160*** | 0.300*** | 0.049* | 0.032 |

| | | (2.875) | (0.333) | (3.246) | (4.031) | (1.840) | |

| Region7 | 7 | 0.178*** | 0.013 | 0.162*** | 0.334*** | 0.053* | 0.098 |

| | | (2.693) | (0.921) | (2.884) | (3.449) | (1.784) | |

| Region9 | 9 | 0.220*** | 0.032 | 0.076* | 0.202*** | 0.100*** | 0.657 |

| | | (2.986) | (1.232) | (2.433) | (3.032) | (2.690) | |

| Xi'an | | | | | | | |

| Region5 | 10 | 0.122** | 0.095 | 0.044* | 0.451*** | 0.024* | 0.002 |

| | | (2.552) | (1.045) | (1.733) | (4.456) | (1.655) | |

| Region 8 | 12 | 0.443*** | 0.103 | 0.145** | 0.092* | 0.232*** | 0.025 |

| | | (3.762) | (1.024) | (2.988) | (1.643) | (3.224) | |

| Shenzhen | | | | | | | |

| Region6 | 13 | 0.055* | 0.002 | 0.105** | 0.188*** | 0.033* | 0.052 |

| | | (1.855) | (0.556) | (4.930) | (2.988) | (1.700) | |

| Region9 | 7 | 0.129** | 0.029 | 0.134*** | 0.090* | 0.115*** | 0.560 |

| | | (1.663) | (2.442) | (4.002) | (1.720) | (2.774) | |

| Notes: * is the significance coefficient , ** is the significance coefficient , *** is the significance coefficient . Linked cities are the number of cities with significant coefficient impacted by the central cities. Coefficient represents the correlation between central city and peripheral cities; coefficient represents the linkage between the peripheral cities in the agglomeration; O-Lag is the regression estimated value of time lag between central city and peripheral cities; W-H T is the Wu-Hausman test, the significance of which means the policy shock of central city on the peripheral cities is not an exogenous variable. |

It could be found that Beijing, Xi'an, Zhengzhou, Shanghai, Wuhan and Shenzhen among the 10 central cities had significant cross-regional policy spillover effects, which incarnated in the wide influences on the cities of other regions and also exerted significant influence on the overall housing transaction of other regions. From the estimation of lag term coefficient, each region was obviously affected by its own historical changes, which was reflected in the statistical significance of the lag term coefficient. From the coefficient and , the regulation policies issued in the 6 central cities had significant impacts on the changes of the housing transaction market in the related regions. The coefficient of deviation between different regions was positive or negative, among which there was a synthetic linkage between the housing markets in the two regions with the positive correlation, and the negative correlation indicated that there was certain substitution effect between the housing markets in the adjacent two regions. The positive correlation indicates that the development between regions is often synchronized, of which the prosperity or recession of one region's real estate market will stimulate another, thus driving its development or weakening. The negative substitution effect indicates that the economic development of different regions and the change of population structure make the population flowing across regions and then lead to the mutual substitution of the housing markets. According to the W-H T test, the impacts of changes caused by the central cities' policies on the associated regions were exogenous variables, and the hypothesis of linkage between regional housing markets were accepted.

For better visualize the cross-regional spillover effect caused by the central cities' real estate policies, spatio-temporal models were constructed respectively using the 6 central cities as policy impact variables and the maximum diffusion range graphs were selected and marked with different colors in each region, let rotation direction represented marginal changes of the overall regional housing market clockwise represent negative and counterclockwise represent positive.

As shown in Figure 5, the significant ripples showing the 6 central cities which had spillover effects spaned a broad range beyond their urban agglomeration classifications. In addition to affecting the Beijing-Tianjin-Hebei region, Beijing's regulatory policies can also spill to northeast, north, northwest and central China; Shanghai's policies can significantly affect the Yangtze River Delta region, but also spread to southward of the Pearl River Delta region and the westward of the middle reaches of the Yangtze River region; Zhengzhou's policies will affect not only the Central Plains but also the middle reaches of the Yangtze River region in the south and parts of the Guanzhong Plains region; The policies issued by Xi'an will also spill to parts of the Central Plains and large area of the middle reaches of the Yangtze River region; Shenzhen's policies were mainly spread to the West Side of Strait agglomeration, even can affect part of the Yangtze River Delta region; Wuhan's policies can spill over to the Chengdu-Chongqing urban agglomeration, the West Side of the Strait agglomeration and part of the Central Plains. Compared with the regional spillover results in Table 1, the central cities' policies had strong cross-regional spillover effects were basically limitation policies, indicating that the restrictive policies were still the most extensive and effective regulation tools for residential market in China. It is undeniable that real estate restrictive policies on developed cities were national policies during the past years, however as we mentioned above in data selection, the results in this study based on the data filtered out the influence of national policies and peripheral cities' local policies, moreover, most of the sample cities which affected by central cities did not strictly implement the restrictive policies, therefore, the conclusions are reliable.

Figure 5 Cross-regional spillover ripples of the 6 central citiesmaximum range |

Full size|PPT slide

4.3 Robustness Test

The explanatory variables in this study come from the identification and quantification of abnormal fluctuations in housing market data. The method of changing explanatory variables is not suitable for the robustness test. Therefore, I did the robustness test by changing the data scale. Respectively use the sum of two months'data and quarterly data to replace the original research data for robustness test, keeping the model setting unchanged, the results show that the significance of the spatio-temporal correlation regression results of the housing market has not changed significantly, indicating the research is robust and reliable. However, the reorganization of data will lead to the losing of fluctuation information, and the quantification of policy impact will be inaccurate. So it was founded that the simulation results were still valid when using the sum of two month's data, but failed by the quarterly data replacement. Excluding the interference of data noise, the conclusion of this study is still robust and reliable. Due to space limitations, the robust results are not listed here.

5 Conclusions and Implications

This study integrates event analysis method on the basis of spatial-temporal model and takes the housing transaction data of 156 prefecture-level cities in 11 major urban agglomerations as research samples to discuss the regional and cross-regional spillover effect of the implementation of 167 items real estate policies in 10 central cities on the peripheral cities. The spillover results are presented in the form of "ripples" in dimensions of time and space, which is conductive to analysis the impact of China's real estate regulation policies on market fluctuations. The research results show that China's housing market has obvious policy-driven characteristics, in which the regulation of some central cities can obviously cause the policy spillover effect in the space and time. This effect is manifested in the policy impact of the central city significantly interfering the the housing market changing of the peripheral cities within the scope of the city, and driving adjacent regions to present gear transmission interactions in the scope of urban agglomeration.

When considering the geographical space factor and taking urban agglomeration as division basis, the regional policy spillover effects of the 10 central cities are as follows: Shenyang had obvious policy spillover effect on the northeast China's housing market, even had a greater impact on the northern cities, in terms of policy types, the influence of consumption-stimulating policies were more effective. Beijing's policies which characterized by significant administrative orders had unexpectedly low influence on the Beijing-Tianjin-Hebei agglomeration, but it had significantly spillover effect on relatively far away cities in Northeast China and Shandong province. Qingdao had relatively limited influence scope to the 3 cities of Jiaodong Peninsula, nor was the spillover effect evident in the provincial capital Jinan. The regulations of Xi'an can form significant spillover effect on Guanzhong Plain area, among which the regulatory policies and restrictive policies were more effective, but with short policy duration. Zhengzhou had short-lived policy spillover effect on the Central Plains with its tax and restrictive policies, but the influence scope was not wide as expected. The influence of Shanghai and Shenzhen was very similar, which restrictive policies had significant spillover effect, but the influence time was not long, and it was easy to trigger the rapid rebound of the market. As one of the pilot cities of real estate tax, Chongqing's real estate tax policy had a certain spillover effect in Chengdu-Chongqing agglomeration, indicating that this region was more sensitive to the collection of real estate tax than Shanghai which was another pilot city. Wuhan had a wide influence on the middle reaches of the Yangtze River area, among which provident fund policies and purchase restriction policies had wide influence but its restrictive policies were easily to form market rebounds, which similar to Shanghai and Shenzhen. Xiamen had wide range impacts on the West Side of the Straits urban agglomeration with many types of policies, among them restrictive policies, loan policies and real estate registration policies all had significant spillover effects, but the lag of their influences were relatively long.

When the geographical space factor is ignored, Beijing, Xi'an, Zhengzhou, Shanghai, Wuhan and Shenzhen among the 10 central cities showed significant cross-regional policy spillover capacities and driven the adjacent region markets produce geared interactions. Among them, Beijing's regulation policies can drive the change of the housing market in the Beijing-Tianjin-Hebei urban agglomeration, and produce an opposite trend of market change in partly the Northeast region, Jiaodong Peninsula and the Central Plains region, and exert a synclastic effect on the Guanzhong Plain region through the Central Plains region. The regulation of Xi'an can affect the Guanzhong Plain urban agglomeration and had a reverse effect on partly agglomerations of the Central Plains and the Middle Reaches of the Yangtze River. Zhengzhou had an influence on the Central Plains, and then exerted reverse effects on the adjacent areas of Guanzhong Plain and the Middle Reaches of the Yangtze River. The regulation of Shanghai can affect the Yangtze River Delta region, and had reverse effect on the adjacent areas of Middle Reaches of the Yangtze River and the West Side of the Straits which respectively exerted reverse influence on the their adjacent Central Plans and Pearl River Delta area. Due to its special geographical location, Wuhan exerted profound reverse effects on the adjacent Central Plains, the West Side of the Straits and Chengdu-Chongqing agglomerations through the Middle Reaches of the Yangtze River area. In addition to influencing the Pearl River Delta area and the West Side of the Straits area, the regulation of Shenzhen also transfered positive impacts on the Yangtze River Delta area which was far away from the geographical location. As for the policy types, the restrictive real estate policies in the above 6 central cities had the most significant spillover effect, indicating that for the housing market, restrictive real estate policies were the most influential and effective regulation and control tools, reflecting the policy-oriented characteristics of China's housing market. In addition, the regional interaction of the housing market also reveals facts that the flow of population and resources in China's regional economy during the past dozen years.

Given the model settings, the limitations of this study are that the spillover direction was unidirectional from the central city to peripheral cities and only one central city in each region was selected in the agglomeration division situation. Future researches will help to improve the model and verify the policy interactions between multiple central cities and more complex regional real estate market interactions in more nuanced region divisions.

{{custom_sec.title}}

{{custom_sec.title}}

{{custom_sec.content}}

PDF(697 KB)

PDF(697 KB)

Figure 1 Market radiation and geared interactions in adjacent regions

Figure 1 Market radiation and geared interactions in adjacent regions Table 1 Policies with strong cross-regional spillover effects

Table 1 Policies with strong cross-regional spillover effects

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}