1 Introduction

The traditional study of option pricing is based on the assumption that the underlying asset obeys the geometric Brownian motion

[1]. However, empirical research on the return on financial assets in recent years shows that financial asset prices are not random walks, but rather fractal features such as self-similarity, long memory and non-periodic cycle. In 1989, Peters

[2] proposed the fractal market hypothesis, applied R/S to analyze different capital markets, and discovered the existence of fractal structures and non-periodic cycles, that is, the price of financial assets depends not only on the current time, but also on the previous historical moment. In general, we use fractional Brownian motion to characterize this self-similarity and long memory.

However, the literature [

3] points out that the fractional Brownian motion is not a semi-martingale, so the classical stochastic analysis theory cannot be directly applied to the fractional Brownian motion, and the direct application of fractional Brownian motion to the financial environment will generate arbitrage opportunities

[4, 5]. Therefore, many scholars began to use modified fractional Brownian motion to describe the behavior pattern of financial asset price changes, such as mixed fractional Brownian motion

[6-8] and bifractional Brownian motion

[9, 10]. Since the bifractional Brownian motion is a Gaussian process that is more extensive than the fractional Brownian motion, it not only has the characteristics of self-similarity and long memory, but also is a semi-martingale under certain restricted conditions, so it can be applied to finance field. The paper [

11] gave the stochastic integral of the bifractional Brownian motion and pointed out that the bifractional Brownian motion can be used to characterize the random volatility of financial assets. In the paper [

12], the author used the geometric bifractional Brownian motion to capture the underlying asset of equity warrants. Moreover, a partial differential equation formulation for valuing equity warrants based on Wick integration was proposed. Meanwhile, the pricing results of different models illustrate that the financial asset had the property of long memory. Zhao

[13] set the asset price followed bifractional Brownian motion, and constructed quasi-martingale method under the risk neutral measure to solve bifractional Black-Scholes model and two kinds of depressed option by the same way. Using the measure transformation method and quasi-martingale technique, the paper [

14] obtained the geometric average Asian call and put option pricing formulas with fixed-price driven by bifractional Brownian motion are generalized. For other studies on bifractional Brownian motion and long memory process can see [

15-

17].

A compound option

[18, 19] is simply an option on an option. The exercise payoff of a compound option involves the value of another option. A compound option then has two expiration dates and two strike prices. There are four main types of compound option, namely, a call on a call, a call on a put, a put on a call and a put on a put. This option has widely been applied in many financial practices. For example, the paper [

20] introduced the concept of multi-stage compound options to the valuation of convertible bonds, and found that adopting the finite difference method to solve the Black-Scholes equation for each stage actually resulted in a better numerical efficiency. In addition, the article

[21] studied the problem of European-style option pricing in time-changed Lévy models in the presence of compound Poisson jumps.

Our paper is organized as follows. Section 2 contains some preliminaries about bifrational Brownian motion. In section 3, a bifractional Black-Scholes equation for European option is derived by the method of Delta hedging strategy and valuation formulas for the European options by variable substitution. It is derived the pricing formula of a call on a call under bifractional Brownian motion by the method of risk neutral pricing when the parameter is greater than 0.5 in section 4, and it can derive the pricing formulas of other compound options in the same manner. Finally, we show that parameter affect risk characteristics of the European options by numerical analysis.

2 Preliminaries

In this section, we first describe some basic facts on the bifractional Brownian motion.

The so-called bifractional Brownian motion with is a mean zero Gaussian process with and the covariance

if , then is the fractional Brownian motion with Hurst parameter .

Now we list some properties of the bifractional Brownian motion by the following proposition.

● The bifractional Brownian motion is self-similar with parameter , i.e., for all ,

● For , the bifractional Brownian motion has long-range dependence in the case that

satisfies

● If and , the bifractional Brownian motion is a semi-martingale;

● The paths of the bifractional Brownian motion are a.s. Hölder continuous with parameter for any .

3 The Bifractional Black-Scholes Equation for European Options

Since bifractional Brownian motion is a well-developed mathematical model of strongly correlated stochastic processes, it is the most efficient tool for capturing the long memory behaviour for the financial asset. firstly, we state some basic assumptions that will be used in this paper.

Consider a financial market with two primitive securities, namely, a risky asset and a risk-free bond . We will need the following assumptions. It is important to note that this article always assumes that the parameters are between and 1.

● The governing stochastic differential equation for the price of a risky asset (such as a stock) is given by

where is the instantaneous expected return of , is its volatility, is the process of the bifractional Brownian motion.

● The price of a risk-free bond is given by

where is a constant risk-free rate.

● There are no transaction costs or taxed and dividends are not paid during the time of outstanding options.

● The market is complete.

Under the risk-neutral measure, we have that

and it is easy to derive that

Lemma 1 Considering a binary differentiable function , is determined by the above stochastic differential equation , we have

Proof According to Taylor's formula, we have

since , we can approximately assume that , then we have that

Ignoring higher order infinitesimal , then the proof is completed.

In the following part, the asset portfolio is constructed, and Black-Scholes partial differential equation driven by bifractional Brownian motion is derived through Delta hedging strategy, then the pricing formula of European options is obtained by the method of boundary-value conditions and variable substitution.

Theorem 1 (Bifractional Black-Scholes Equation) Suppose is the price of the European call option at time t, and the price of the underlying asset satisfies , then satisfies the following partial differential equation

Proof Construct a self-financing portfolio : Buy one unit a European call option and sale units underlying assets, i.e., . According to lemma 1, we can know that

Choose so that the portfolio is risk-free at , that is .

Let , we have

Then (7) is obtained, the proof is completed.

Theorem 2 Assuming that the maturity date is and the strike price is , the price of the European call option under the bifractional Brownian motion at any time is

where is the cumulative standard normal distribution function and

Proof According to Theorem 1, is defined by Theorem 1, and the boundary-value condition is .

Let , then we get

Substituting (11) into (7), we get

and the boundary-value condition becomes .

Let and , then we have

Substituting (13) and (14) into (12), the following heat equation is obtained.

where the boundary-value condition is .

According to the classical solution theory of heat equation, (15) has a unique strong solution, which is described by the following form

substituting the boundary-value condition into (16), we can get

By the inverse transformation, we can derive the formula of the European call option in the bifractional Black-Scholes model, and the proof is completed.

At the same way, we can obtain the formula of the European put option.

Theorem 3 Assuming that the maturity date is , the strike price is and is defined by , then the price of European put option at any time is

where and are the same as the above.

Corollary 1 The put-call parity formula for the bifracitonal Brownian motion can be written as the following form

4 The Pricing Formulas of Compound Options

In this section we consider a compound option(a call on a call) with strike price and maturity , which terminal payoff is

where denotes the stock price at time , is the price value of a European call option and .

Based on these assumptions, we know that at time this option gives the right to buy another call option and at time this call option gives the right to buy the stock. Now we derive the pricing formulas of this compound option.

Lemma 2 (see [

22])

Let denotes the quasi-conditional expectation with respect to the risk-neutral measure, the price at every time of the claim is given by

Theorem 4 (a call on a call) The value of this compound option at time is

where

and are the same as the above, denotes the two dimensional cumulative standard normal distribution function with correlation coefficient .

Proof Let denotes the value of a European call option, according to Theorem 2, we know that

where .

Let , then satisfies the following equation

where

and the exercise condition of this compound option obviously is .

According to risk-neutral principle and Lemma 2, the value of this compound option is the expected present value as follows:

where and denotes the indicator function.

Noted that

then we obtain that

So we can derive that .

Due to , where

so we have that

where

then

and the proof is completed.

By the similar argument, we may obtain the results on the other compound options(a call on a put, a put on a call and a put on a put, respectively). The following theorems are given without proof.

Theorem 5 (a put on a call) The value of this compound option at time is

Theorem 6 (a call on a put) The value of this compound option at time is

Theorem 7 (a put on a put) The value of this compound option at time is

5 Numerical Simulation Analysis of Risk Characteristics

Among many risk characteristic parameters, and are the two most important indexes of option pricing sensitivity. is the slope of the option value, also known as the hedging ratio, which accurately defines how many units the option price will change when the underlying asset price changes by one unit. This sensitivity is what option investors are most concerned about. When constructing the risk-free arbitrage asset portfolio, the ratio of the underlying asset held by the investor to the option position is . is the curve of the option value line. The larger is, the harder it is to avoid risk. In this paper, the Black-Scholes option pricing model is taken as an example to analyze the risk characteristics. According to formula (10), the two hedging parameters can be deduced as follows:

where .

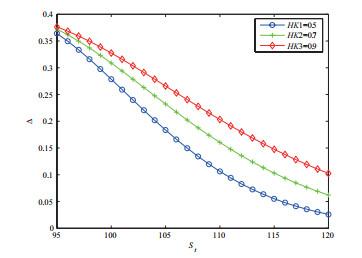

We take a first look at the value of for different parameters . Apparently, in the case displayed in Figure 1, an increasing parameter comes along with a increasing of the value of . Noticed that the value of is positive, which is consistent with the characteristics of European call options. It's easy to see that the value of is negative when the option is European put option.

Figure 1 The value of with varying parameter () |

Full size|PPT slide

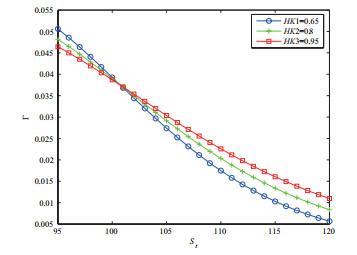

Figure 2 indicates that decreases with the increase of when the price of the underlying asset is not much different from the exercise price . When differs greatly from , is proportional to . This indicates that the investors are more willing to exercise this option when the difference between and is large, otherwise, this option will not be exercised.

Figure 2 The value of with varying parameter () |

Full size|PPT slide

6 Conclusions

A large number of scholars have shown that the price volatility of financial assets has a long memory, which leads to the improvement of option pricing model based on Brownian motion hypothesis. In this paper, the Black-Scholes option pricing formula driven by bifractional Brownian motion is solved by Delta hedging strategy. Furthermore, we study the European options and the compound options driven by the bifractional Brownian motion respectively. By comparing the fluctuation of risk characteristics under different values, it is found that European call options with higher long memory parameter are more conducive to investors to implement effective hedging strategies.

{{custom_sec.title}}

{{custom_sec.title}}

{{custom_sec.content}}

PDF(167 KB)

PDF(167 KB)

Figure 1 The value of

Figure 1 The value of

{kind=link}

{kind=link}