PDF(7136 KB)

PDF(7136 KB)

What is the Industrial Structure Changes of China?

Yijie WANG, Yanyan KE, Xianrui MA, Yitian REN

Journal of Systems Science and Information ›› 2020, Vol. 8 ›› Issue (6) : 487-503.

PDF(7136 KB)

PDF(7136 KB)

What is the Industrial Structure Changes of China?

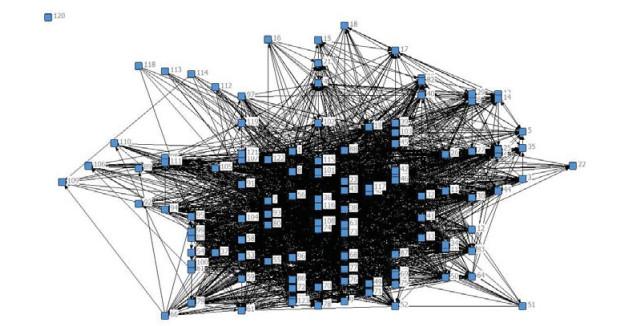

Although China has made great achievements in economic scale, the model of high-quality economic developments is still in the exploratory stage. A series problems, such as unreasonable industrial structure and low production efficiency, need to be resolved urgently. The transformation and upgrading of industrial structure is the inevitable choice. The analysis of industrial relations is an important method to reveal the internal mechanism of industrial structure change. Therefore, based on the concepts of sensitivity and influence coefficient, this paper proposed the concepts of driven and driving coefficient, and constructed the industrial complex networks of China from 1999 to 2013 according to the EORA input-output table. From the perspectives of the interaction power, industrial linkages and community structure, this paper systematically analyzes the evolution of China's industrial structure. Results show that China's industrial structure is undergoing a transformation from industry-oriented to industry-service-oriented. The interaction linkages between industries has formed a robust association structure. The traditional sectors such as infrastructure construction and industries are still the largest consumer group driving the development of other industries. Besides, light industry, infrastructure construction and finance have become increasingly important hub industries in the industrial system. However, some unbalanced community structures are formed in the economic system, which has resulted in a waste of resources and low production efficiency to a certain extent. Effectively grasping the relationship between China's industrial structure evolution and its association is conducive to formulating economic restructuring policies, promoting the upgrading of China's economic and, realizing the leap from quantitative change to qualitative change.

industrial structure / driven and driving ability / complex network / community structure {{custom_keyword}} /

Table 1 The industrial sectors with top ten driving and driven coefficient |

| Year | Driven coefficient | Year | Driving coefficient | |

| 2013 | 62, 67, 70, 71, 72, 73, 74, 77, 78, 81 | 2013 | 9, 10, 11, 12, 38, 39, 58, 59, 85, 123 | |

| 2012 | 62, 67, 70, 71, 72, 73, 74, 77, 78, 81 | 2012 | 11, 37, 39, 69, 70, 91, 92, 94, 103, 106 | |

| 2011 | 62, 67, 70, 71, 72, 73, 74, 77, 78, 81 | 2011 | 9, 10, 12, 38, 58, 59, 70, 85, 97, 103 | |

| 2010 | 62, 67, 70, 71, 72, 73, 74, 77, 78, 81 | 2010 | 9, 10, 12, 38, 58, 59, 70, 85, 97, 103 | |

| 2009 | 62, 67, 70, 71, 72, 73, 74, 77, 78, 81 | 2009 | 9, 10, 12, 38, 58, 59, 70, 85, 97, 103 | |

| 2008 | 62, 67, 70, 71, 72, 73, 74, 77, 78, 81 | 2008 | 9, 10, 12, 38, 58, 59, 70, 85, 97, 103 | |

| 2007 | 62, 67, 70, 71, 72, 73, 74, 77, 78, 81 | 2007 | 9, 10, 12, 38, 58, 59, 70, 85, 97, 103 | |

| 2006 | 44, 45, 46, 49, 67, 70, 71, 74, 77, 84 | 2006 | 10, 12, 38, 44, 58, 59, 70, 85, 103, 123 | |

| 2005 | 44, 45, 46, 49, 67, 70, 71, 74, 77, 84 | 2005 | 10, 12, 38, 44, 58, 59, 70, 85, 97, 103 | |

| 2004 | 44, 45, 46, 49, 62, 67, 70, 71, 74, 77 | 2004 | 10, 12, 38, 44, 58, 59, 70, 85, 97, 103 | |

| 2003 | 44, 45, 46, 49, 62, 67, 70, 71, 77, 84 | 2003 | 10, 12, 38, 44, 58, 59, 70, 85, 97, 103 | |

| 2002 | 44, 45, 46, 49, 62, 67, 70, 71, 77, 84 | 2002 | 10, 12, 38, 44, 58, 59, 70, 85, 97, 103 | |

| 2001 | 28, 42, 44, 45, 46, 49, 62, 70, 74, 77 | 2001 | 10, 12, 38, 44, 58, 59, 70, 85, 97, 103 | |

| 2000 | 28, 42, 44, 45, 46, 49, 62, 67, 70, 74 | 2000 | 10, 12, 38, 44, 58, 59, 70, 85, 97, 103 | |

| 1999 | 28, 42, 44, 45, 46, 49, 62, 67, 70, 77 | 1999 | 10, 12, 38, 44, 58, 59, 70, 85, 97, 103 |

Table 2 The top 25 sectors ranked by the betweenness centrality |

| Sector | Betweenness | nBetweenness | Sector | Betweenness | nBetweenness | |

| 85 | 746.956 | 5.06 | 74 | 227.962 | 1.544 | |

| 104 | 551.099 | 3.733 | 46 | 205.631 | 1.393 | |

| 63 | 493.7 | 3.344 | 30 | 197.129 | 1.335 | |

| 36 | 490.02 | 3.319 | 32 | 193.822 | 1.313 | |

| 73 | 463.187 | 3.138 | 48 | 181.091 | 1.227 | |

| 60 | 439.994 | 2.981 | 39 | 178.503 | 1.209 | |

| 37 | 433.495 | 2.937 | 103 | 176.241 | 1.194 | |

| 56 | 418.356 | 2.834 | 77 | 173.862 | 1.178 | |

| 91 | 410.269 | 2.779 | 33 | 168.671 | 1.143 | |

| 84 | 392.539 | 2.659 | 97 | 157.857 | 1.069 | |

| 99 | 375.422 | 2.543 | 58 | 157.322 | 1.066 | |

| 23 | 351.485 | 2.381 | 93 | 155.221 | 1.051 | |

| 101 | 282.688 | 1.915 |

Table 3 The density of Cohesion subgroup for 123 sectors in China in 2013 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

| 1 | 0.739 | 0.733 | 0.952 | 1 | 0.778 | 0.736 | 0.901 | 0.981 |

| 2 | 0.367 | 0.5 | 0.657 | 0.7 | 0.168 | 0.45 | 0.57 | 0.629 |

| 3 | 0.238 | 0.057 | 0.476 | 0.69 | 0.083 | 0 | 0.317 | 0.762 |

| 4 | 0.5 | 0.533 | 0.929 | 0.967 | 0.439 | 0.275 | 0.846 | 0.976 |

| 5 | 0.032 | 0.032 | 0.015 | 0.026 | 0.07 | 0.034 | 0.037 | 0.015 |

| 6 | 0.061 | 0.06 | 0.064 | 0.033 | 0.097 | 0.221 | 0.033 | 0.026 |

| 7 | 0.041 | 0.022 | 0.032 | 0.049 | 0.07 | 0.013 | 0.051 | 0.028 |

| 8 | 0.114 | 0.019 | 0.19 | 0.238 | 0.043 | 0.012 | 0.219 | 0.462 |

Table 4 Sectors with a pull coefficient and a push coefficient greater than 1 between 1999 and 2013 |

| Code | Sector | Code | Sector | |

| 23 | Cotton textiles | 56 | Steel-processing | |

| 33 | Printing and record medium reproduction | 57 | Alloy iron smelting | |

| 36 | Petroleum refining | 58 | Nonferrous metal smelting | |

| 37 | Coking | 59 | Nonferrous metal processing | |

| 38 | Raw chemical materials | 63 | Other general industrial machinery | |

| 41 | Chemicals for painting, dying and others | 68 | Vehicles fittings production | |

| 42 | Synthetic chemicals | 69 | Ship building | |

| 43 | Chemicals for special usages | 84 | Scrap and waste | |

| 46 | Chemical fibers | 85 | Electricity and steam production and supply | |

| 47 | Rubber products | 90 | Railway freight transport | |

| 48 | Plastic products |

| Code | Sector | Code | Sector | |

| 1 | Crop cultivation | 63 | Other general industrial machinery | |

| 2 | Forestry | 64 | Agriculture, forestry, animal husbandry and fishing machinery | |

| 3 | Logging and transport of timber, bamboo | 65 | Other special industrial equipment | |

| 4 | Livestock, its products | 66 | Railroad transport equipment | |

| 5 | Fishery | 67 | Motor vehicles | |

| 6 | Technical services for agriculture, forestry, livestock, fishing | 68 | Vehicles fittings production | |

| 7 | Coal mining and processing | 69 | Ship building | |

| 8 | Crude petroleum products, Natural gas products | 70 | Other transport machinery | |

| 9 | Ferrous ore | 71 | Generators | |

| 10 | Non-ferrous ore mining | 72 | Household electric appliances | |

| 11 | Salt mining | 73 | Other electric machinery and equipment | |

| 12 | Non-metal minerals and other mining | 74 | Communication equipment | |

| 13 | Grain mill products | 75 | Electronic computer | |

| 14 | Feeding stuff production and processing | 76 | Other computer devices | |

| 15 | Vegetable oil and forage | 77 | Electronic element and device | |

| 16 | Sugar refining | 78 | Electronic appliances | |

| 17 | Slaughtering, meat, eggs and dairy products | 79 | Other electronic and communication equipment | |

| 18 | Prepared fish and seafood | 80 | Instruments, meters and other measuring equipment | |

| 19 | Other food products | 81 | Cultural and office equipment | |

| 20 | Wines, spirits and liquors | 82 | Arts and crafts products | |

| 21 | Non-alcoholic beverage | 83 | Other manufacturing products | |

| 22 | Tobacco products | 84 | Scrap and waste | |

| 23 | Cotton textiles | 85 | Electricity and steam production | |

| 24 | Woolen textiles | 86 | Gas production and supply | |

| 25 | Hemp textiles | 87 | Water production and supply | |

| 26 | Other textiles not classified | 88 | Construction | |

| 27 | Knitted mills | 89 | Railway passenger transport | |

| 28 | Wearing apparel | 90 | Railway freight transport | |

| 29 | Leather, furs, related products | 91 | Highway freight and passengers transport | |

| 30 | Sawmills and fibreboard | 92 | Domestic public transport | |

| 31 | Furniture and products of wood, etc. | 93 | Water freight and passengers transport | |

| 32 | Paper and products | 94 | Air passenger transport | |

| 33 | Printing and record medium reproduction | 95 | Air freight transport | |

| 34 | Cultural goods | 96 | Pipeline transport | |

| 35 | Toys, sporting and athletic | 97 | Warehousing | |

| 36 | Petroleum refining | 98 | Post | |

| 37 | Coking | 99 | Telecommunication | |

| 38 | Raw chemical materials | 100 | Computing services and software | |

| 39 | Chemical fertilizers | 101 | Wholesale and retail trade | |

| 40 | Chemical pesticides | 102 | Hotels | |

| 41 | Chemicals for painting, dying and others | 103 | Eating and drinking places | |

| 42 | Synthetic chemicals | 104 | Finance | |

| 43 | Chemicals for special usages | 105 | Insurance | |

| 44 | Chemical products for daily use | 106 | Real estate | |

| 45 | Medical and pharmaceutical products | 107 | Leasehold | |

| 46 | Chemical fibers | 108 | Business services | |

| 47 | Rubber products | 109 | Tourism | |

| 48 | Plastic products | 110 | Scientific research | |

| 49 | Cement and cement asbestos products | 111 | General technical services | |

| 50 | Glass and glass products | 112 | Geological prospecting | |

| 51 | Pottery, China and earthenware | 113 | Water conservancy | |

| 52 | Fireproof products | 114 | Environmental resources and public infrastructure | |

| 53 | Other non-metallic mineral products | 115 | Resident services and other services | |

| 54 | Iron-smelting | 116 | Educational services | |

| 55 | Steel-smelting | 117 | Health services | |

| 56 | Steel-processing | 118 | Social welfare | |

| 57 | Alloy iron smelting | 119 | Culture and arts, radio, film and television | |

| 58 | Nonferrous metal smelting | 120 | Sports | |

| 59 | Nonferrous metal processing | 121 | Recreational services | |

| 60 | Metal products | 122 | Public administration and other sectors | |

| 61 | Boiler, engines and turbine | 123 | Re-export & Re-import | |

| 62 | Metalworking machinery |

| 1 |

Ye M, Wu J Q. Connotation and development of new-type building industrialization. China Construction News, 2013-02-26(005).

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 2 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 3 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 4 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 5 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 6 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 7 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 8 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 9 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 10 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 11 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 12 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 13 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 14 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 15 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 16 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 17 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 18 |

Li H Y, Chi Y Y, Li J L, et al. Effect factors of China's industry structure based on redundancy analysis. International Conference on Machine Learning & Cybernetics, 2015.

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 19 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 20 |

Hioki S, Hewings G, Okamoto N. Identifying the structural changes of China's spatial production linkages using a qualitative input-output analysis. Journal of Econometric Study of Northeast Asia, 2005: (6). Avaiable online: https://www.researchgate.net/publication/251350375_Identifying_the _Structural_Changes_of_China's_Spatial_Production_Linkages_Using_a_Qualitative_Input-Output_Analysis.

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 21 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 22 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 23 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 24 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 25 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 26 |

Boar R G, Iovanovici A, Ciocarlie H, et al. Complex network interpretation of European Union economic dynamics. IEEE International Symposium on Applied Machine Intelligence and Informatics, 2017.

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 27 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 28 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 29 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 30 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 31 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 32 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 33 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 34 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 35 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 36 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 37 |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| 38 |

Guo Y, Xue Y. Research on cooperative relations for identifying abnormal vertices in complex financial networks. International Conference on Electronic Commerce and Business Intelligence, 2009.

{{custom_citation.content}}

{{custom_citation.annotation}}

|

| {{custom_ref.label}} |

{{custom_citation.content}}

{{custom_citation.annotation}}

|

PDF(7136 KB)

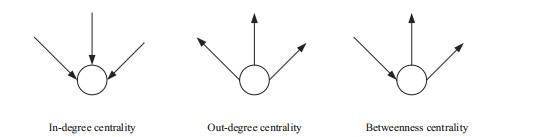

Figure 1 The degree centrality and betweenness centrality in complex network

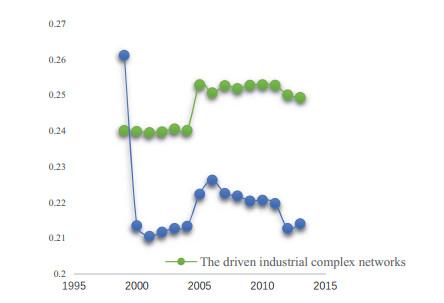

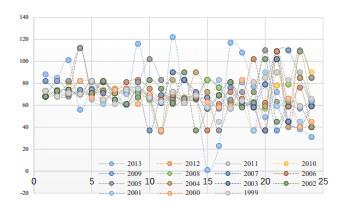

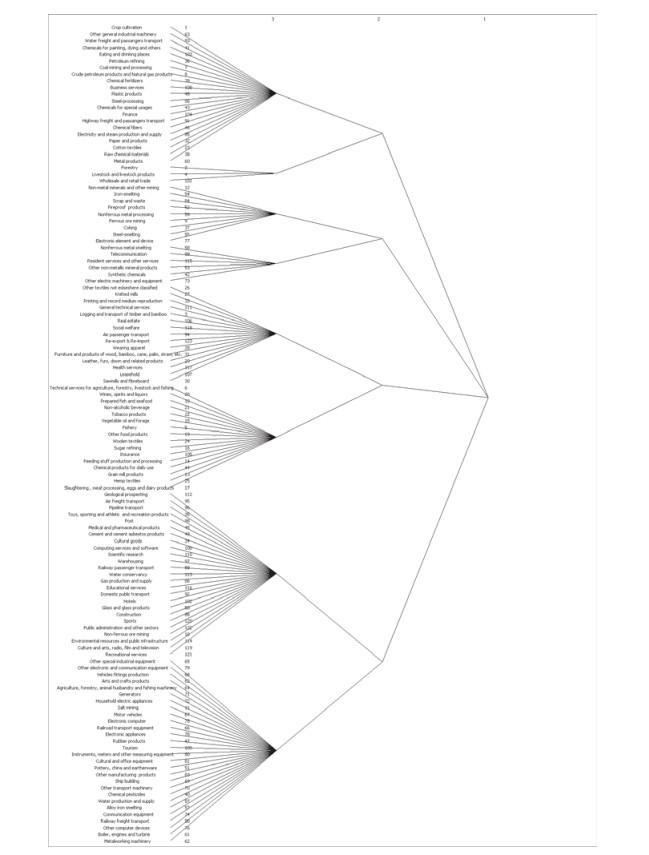

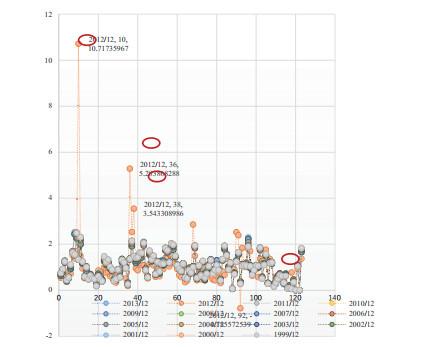

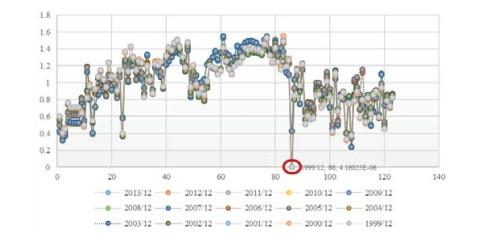

Figure 1 The degree centrality and betweenness centrality in complex network Table 1 The industrial sectors with top ten driving and driven coefficientFigure 2 The topology network of China's industrial sectorsFigure 3 The densities of driven and driving industrial complex networksFigure 4 The top 25 sectors ranked by point-outFigure 5 The top 25 sectors ranked by point-inTable 2 The top 25 sectors ranked by the betweenness centralityFigure 6 Industrial symbiosis block division in China in 2013Table 3 The density of Cohesion subgroup for 123 sectors in China in 2013Figure 7 The changes of driving coefficientFigure 8 The changes of driven coefficientsTable 4 Sectors with a pull coefficient and a push coefficient greater than 1 between 1999 and 2013

Table 1 The industrial sectors with top ten driving and driven coefficientFigure 2 The topology network of China's industrial sectorsFigure 3 The densities of driven and driving industrial complex networksFigure 4 The top 25 sectors ranked by point-outFigure 5 The top 25 sectors ranked by point-inTable 2 The top 25 sectors ranked by the betweenness centralityFigure 6 Industrial symbiosis block division in China in 2013Table 3 The density of Cohesion subgroup for 123 sectors in China in 2013Figure 7 The changes of driving coefficientFigure 8 The changes of driven coefficientsTable 4 Sectors with a pull coefficient and a push coefficient greater than 1 between 1999 and 2013/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}